摘要

在我国经济结构转型的大背景下,越来越多的上市公司选择通过并购来实现优质资产整合与产业升级转型。与其他企业日常的投融资活动不同,并购交易事务繁杂、专业性强、交易双方信息不对称显著,非专业人士很难对企业并购的协同效应与相关交易风险进行准确评估,因此,许多上市公司选择聘用具有丰富证券从业经验的董事以快速获取相关经验与人脉关系。据统计,2008-2015 年期间,全部 A 股上市公司中 35.58%的公司具有证券背景董事,即便剔除金融行业与房地产行业,这一占比仍高达 33.80%。基于这一普遍存在的现象,本文试图对董事的证券背景与企业并购绩效的关系进行

探究,其中,董事的证券背景是董事从业背景中的一种,企业并购绩效是公司投资决策效果的重要衡量方式,两者之间的关系是董事从业背景对企业对外投资的咨询作用的具体体现。现有关于董事背景的研究主要集中于政府及商业银行从业背景,对证券背景鲜有涉猎,而董事的证券背景所具有的知识储备与人脉关系高度契合于企业并购过程中的资源需求,因此,对于两者关系的研究具有较强的理论与实践意义。

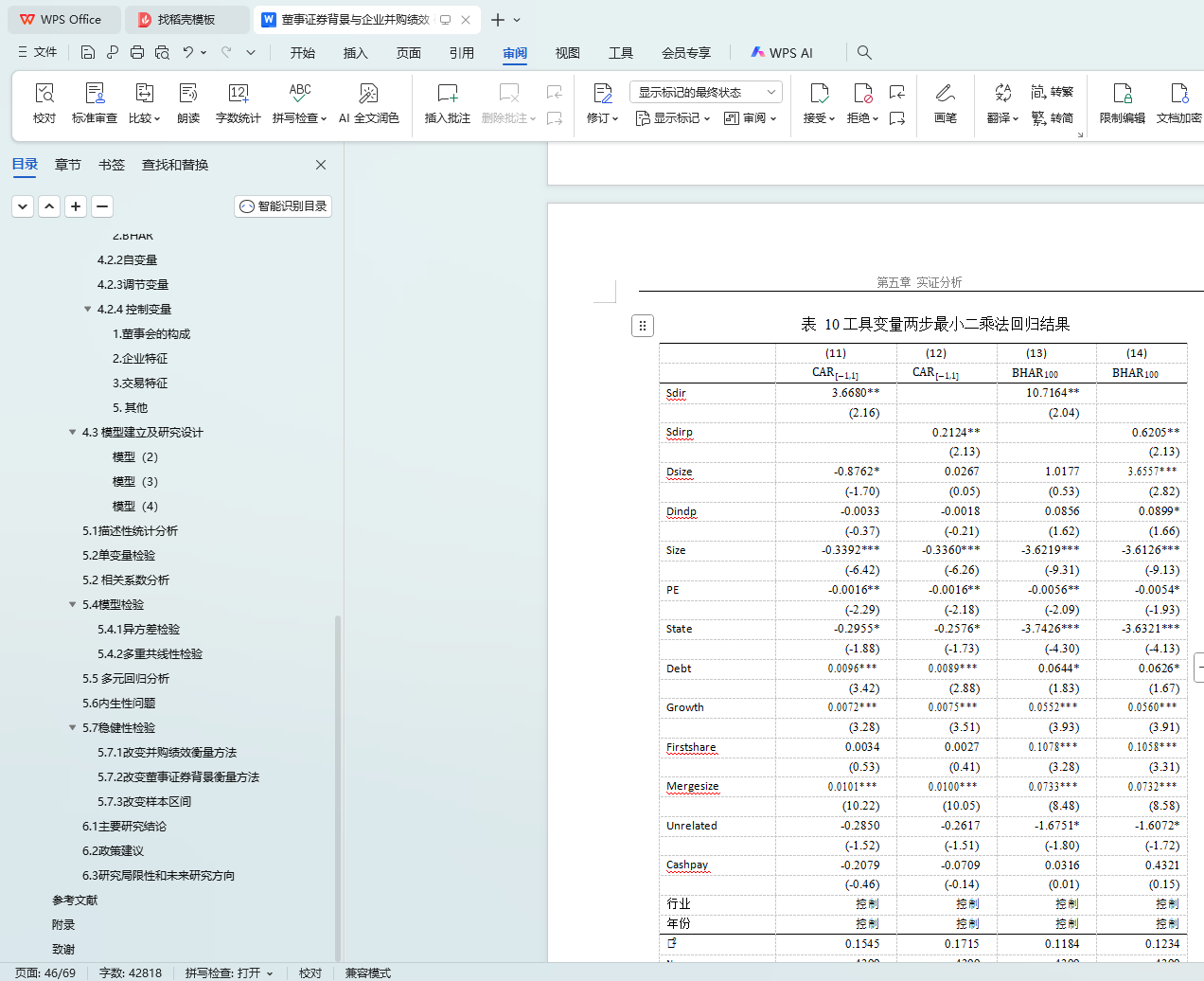

在系统梳理中外相关文献的基础上,本文以 2008-2015 年上市公司并购事件作为样本,研究了董事证券背景对于企业并购绩效是否可以发挥有效的咨询职能,并探究董事咨询能力及并购交易本身的咨询需求对于其职能发挥的影响。结果表明,证券背景董事可显著提升企业并购绩效,其他条件相同时,具有证券背景董事的公司相比于不具有证券背景董事的公司,其短期并购绩效CAR[−1,1]可提升 0.5766 个百分点,相当于样本内全部并购事件平均CAR[−1,1]水平的 29.31%。对于影响咨询职能发挥的因素,本文结果表明,兼职多和具有大型券商工作经历的证券背景董事具有更强的咨询能力, 对并购绩效的提升作用更强;非关联并购相较于关联并购对董事咨询职能的需求更高, 证券背景董事对于非关联并购绩效的提升作用更显著。

本文从董事咨询职能角度验证了董事证券背景对于企业并购绩效的提升作用,不仅丰富了董事背景相关研究文献,更为企业董事会结构的优化及投资者投资组合的构建提供了理论基础。

关键词:董事咨询职能,董事证券背景,并购绩效

Directors’ Working Experience in Securities Industry and Firm’s M&A Performance

Wang Dan (Finance) Directed by Cen Wei

ABSTRACT

In the context of China's economic restructuring, more and more listed companies choose to use acquisitions to consolidate high-quality asset or complete industrial upgrading. Different from other daily investment and financing decisions, M&A deals are of great information asymmetry and complexity. Lots of public firms choose to dominate directors with working experience in securities industy (“Securities Directors” for short) to help them evaluate the synergies and risks of acquisions. According to our sample, 35.58% of Chinese listed companies have Securities Directors. The propotion is up to 33.8% even after excluding financial and real estate firms. Their prior experience and rich personal network will promote firm’s target selection and capital operation.

Based on this common phenomenon, this paper examines whether directors’ past working experience in securities companies will enhance board effectiveness and improve the quality of firm’s acquisitions. Their relationship is one of the reflection of board of directors’ advising role on firm’s decision making. Untill now, most relevant papers paid their attention to directors’ political connection or employment history of commertial bank. However, Securities Directors who are most relevant to firm’s M&A performance are rarely researched. So exploring their relationship is of strong theoretical and practical significance.

Based on a smple of Chinese A-share’s M&A activities between 2008 and 2015, we conjecture that Securities Directors are positively related to firm’s subsequent acquisition performance. The company with Securities Directors can experience 0.5766% higher cumulative abnormal return (CAR[-1,1]) which equals to 29.31% of the average CAR[-1,1]. After proving the existence of Securities Directors’ positive advising role on firm’s M&A process. We futher exploered whether directors’ advisory ability and deal’s advisory demand will affect their infulence. The empirical results indicate Securities Directors with working experience in big securities companies or have larger social network will perform their duty better. And compared with the related M&A deals which have low consulting demand, Securities

Directors do a better job on unrelated M&A deals.

From the perspective of directors’ advisory role, this paper suggest firms will be better served on M&A decisions to select Securities Directors who have rich securities expertise and social network. This research not only enriches relevant literature, but also provides theoretical foundation for optimization of board structure and construction of investment portfolio.

KEY WORDS: director’s work experience in securities industry, M&A performance, director’s advisory function,