繁忙董事会与公司风险承担摘要

自 2008 年美国金融危机之后,人们越来越意识到在评价公司业绩表现时不应该忽

略其承担的风险。越来越多的学者也不再仅仅关注公司的业绩表现,也将视角逐渐转向公司的风险。传统的委托代理理论认为经理层出于对职业地位与财富稳定的考虑, 是风险厌恶的。也有行为决策理论认为当决策权过于集中在经理层手上,经理层易于做出偏激的决策,加大公司的风险。虽然不应一概而论地判断公司风险承担的好坏, 但如果一味地追求高收益而采取冒进的策略,会使公司陷入高风险之中;当然,如果公司风险承担水平过低,固步自封,也不利于公司的进一步开拓和创新,其结果也将损害股东的价值。风险决策是公司经营决策的一个重要组成部分,过高或过低的风险水平通常与公司的治理效率有关。

董事会治理是现代企业公司治理中重要组成部分,董事会人员架构与人员特质对董事会职能的发挥至关重要。作为公司的最高决策层,董事会要参与公司的战略制定、实施;董事会的另一主要职能之一就是代替股东监督管理层,谋求股东利益最大化。然而截至 2014 年,约有 93.84%的 A 股上市公司中存在连锁董事,有一些董事甚至同时成为 6、7 家公司的董事会成员,这不禁让人们对其职责履行的有效性存疑。

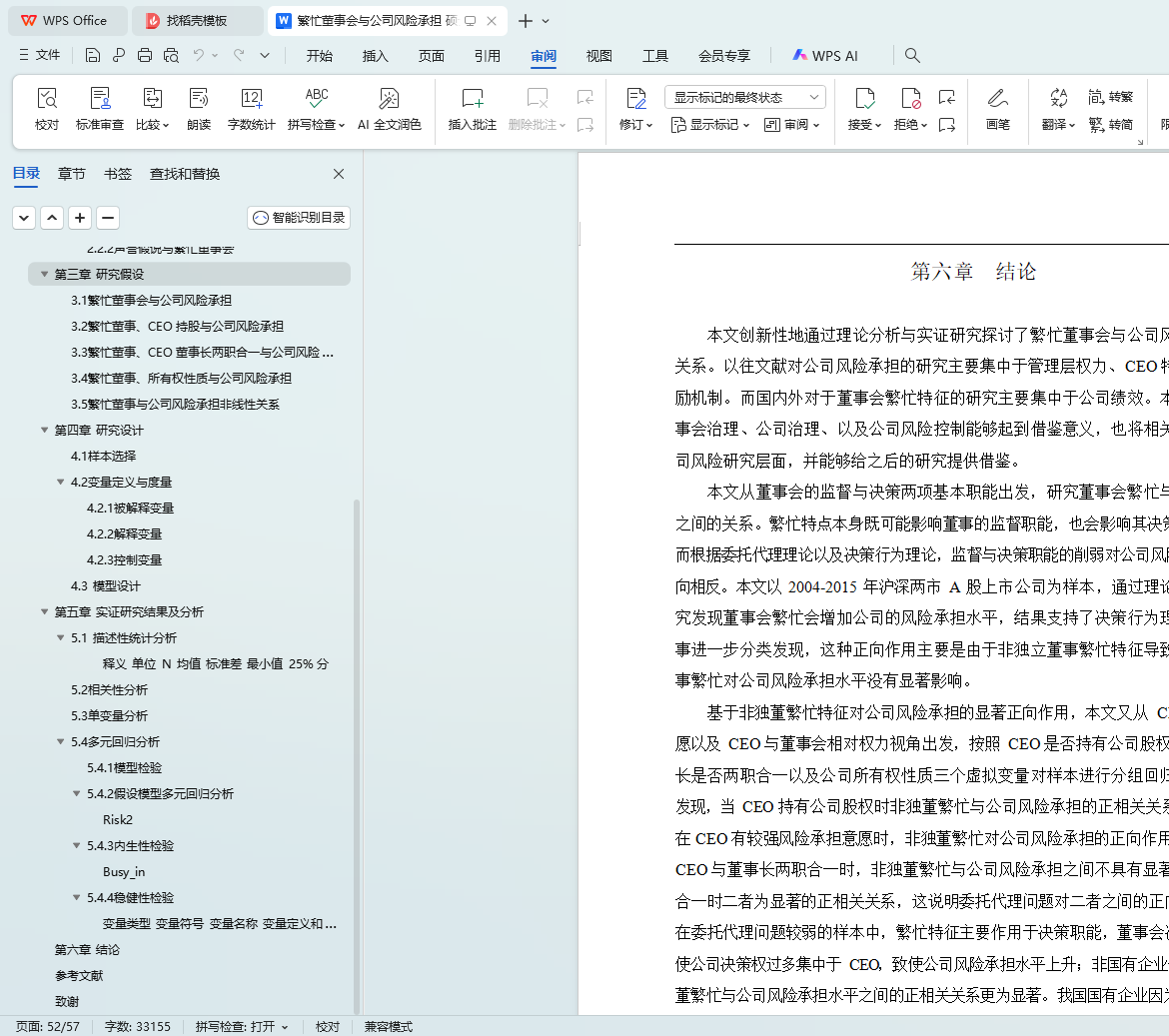

本文希望通过董事会繁忙这一特征出发,研究其与公司风险承担之间的关系,并探讨在不同情况下董事会繁忙与公司风险承担之间的关系。本文以 2004-2015 年沪深两市 A 股上市公司为样本,通过理论分析与实证研究发现董事会繁忙会增加公司的风险承担水平,结果支持了决策行为理论。并且这种正向作用主要是由于非独立董事繁忙特征导致的,而独立董事繁忙对公司风险承担水平没有显著影响。

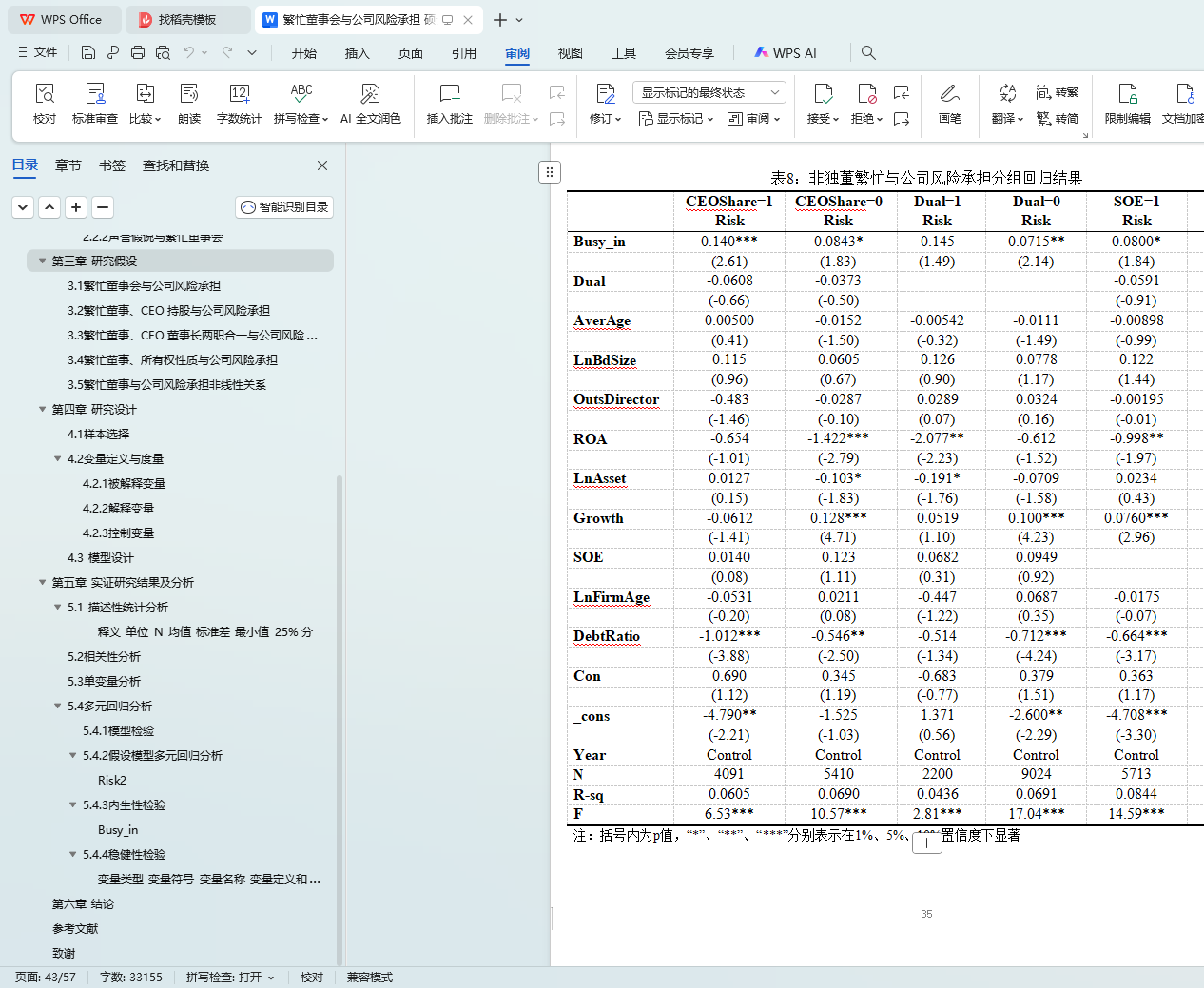

基于非独董繁忙特征对公司风险承担的显著正向作用,本文又从 CEO 风险承担意愿以及 CEO 与董事会相对权力视角出发,按照 CEO 是否持有公司股权、CEO 与董事长是否两职合一以及公司所有权性质三个虚拟变量对样本进行分组回归。进一步研究发现,当 CEO 持有公司股权时非独董繁忙与公司风险承担的正相关关系更显著;当

CEO 与董事长两职合一时,非独董繁忙与公司风险承担之间不具有显著关系,两职不

合一时二者为显著的正相关关系;非国有企业分组中,非独董繁忙与公司风险承担水平之间的正相关关系更为显著。

由于繁忙特征会既会影响董事会的监督职能又会影响其决策职能,基于委托代理理论与行为决策理论,二者对公司风险承担的作用相反,本文进一步研究发现非独董繁忙程度与公司风险承担具有倒 U 的关系,当非独董繁忙人数占比超过 48.91%时,非独董繁忙程度与公司风险承担开始呈现显著负相关关系,目前我国非独董繁忙程度较低,还处于拐点左侧的递增区间。

关键词:繁忙董事会、风险承担、CEO 持股、CEO 董事长两职合一、所有权性质

Busy Boards and Corporate Risk-Taking

Lv Xinmeng ( Finance ) Directed by Prof. Cen Wei

ABSTRACT

Since the American financial crisis in 2008, people increasingly realized that when evaluating corporate performance, risk-taking should also be considered. More and more scholars also started studying corporate risk-taking. Traditional principal-agent theory points that CEOs are risk averse, and they tend to take risk avoidance strategies to keep their jobs and wealth. However, based on the view of power balance, behavioral decision theory points that the bigger the managers’ power is, the higher the corporate risk-taking will be. Well if blindly pursue high yield and take aggressive strategy, it will trap corporate into high risk. But if risk-taking level is too low, corporates may miss good investment opportunities and it will also harm the corporate value. Risk decision is crucial for company management. Too high or too low risk-taking level is often associated with corporate governance efficiency.

The board governance is an important part in corporate governance. As the company's top executives, the board directors participate in the company strategy development and implementation; Directors should also supervise managers to maximize shareholders’ interests. In 2014, 93.84% companies have interlock directors, some directors even serve seven different boards. It may affect the corporate governance efficiency.

This paper aims to study the correlation between the corporate risk-taking and multiple directorships. This paper chooses 2075 companies listed in Shanghai and Shenzhen Stock Exchange as samples, and the time is from 2005 to 2014. Through theoretical and empirical research, it concludes that busy boards increase the corporate risk-taking level, which supports the behavioral decision theory. Moreover, busy independent directors do not influence the risk-taking level. It is the busy inside directors that increase the corporate risk-taking level.

Furthermore, this paper also concludes that when CEOs hold the stock shares of the companies, the positive correlation between the busy inside directors and corporate

risk-taking level is more significant. When CEOs duality leadership exists, the positive correlation between the busy inside directors and corporate risk-taking level is not significant. Among the state-owned companies, the positive correlation is less significant than others.

As the multiple directorships may affect the quality of managerial oversight as well as decision development. Based on the principal-agent theory and behavioral decision theory, they may influence the corporate risk-taking level oppositely. Empirical research shows evidence that busy inside directors and risk-taking level have nonlinear relationship, and more specifically, inverted u-shaped relationship. When the proportion of the busy inside directors is less than 48.91%, the proportion is positively correlated with corporate risk-taking level. And when the proportion is over 48.91%, the correlation begins to be negative. Due to the relatively low proportion of busy inside directors in Chinese listed companies, the positive correlation is dominant.

Key Words: busy boards, risk-taking, CEO share-holding, CEO duality leadership, ownership structure

目录

摘要 I

ABSTRACT III

目录 V

第一章 引言 1

1.1 研究背景 1

1.2 研究意义与贡献 2

1.3 研究内容与框架 3

第二章 文献回顾 5

2.1 公司风险承担研究综述 5

2.1.1 委托代理理论与公司风险承担 5

2.1.2 行为决策理论与公司风险承担 8

2.1.3 关于公司风险承担其他研究成果 10

2.2 繁忙董事会研究综述 11

2.2.1 繁忙假说与繁忙董事会 11

2.2.2 声誉假说与繁忙董事会 12

第三章 研究假设 14

3.1 繁忙董事会与公司风险承担 14

3.2 繁忙董事、CEO 持股与公司风险承担 15

3.3 繁忙董事、CEO 董事长两职合一与公司风险承担 15

3.4 繁忙董事、所有权性质与公司风险承担 16

3.5 繁忙董事与公司风险承担非线性关系 16

第四章 研究设计 17

4.1 样本选择 17

4.2 变量定义与度量 17

4.2.1 被解释变量 17

4.2.2 解释变量 18

4.2.3 控制变量 19

4.3 模型设计 23

第五章 实证研究结果及分析 24

5.1 描述性统计分析 24

5.2 相关性分析 27

5.3 单变量分析 29

5.4 多元回归分析 29

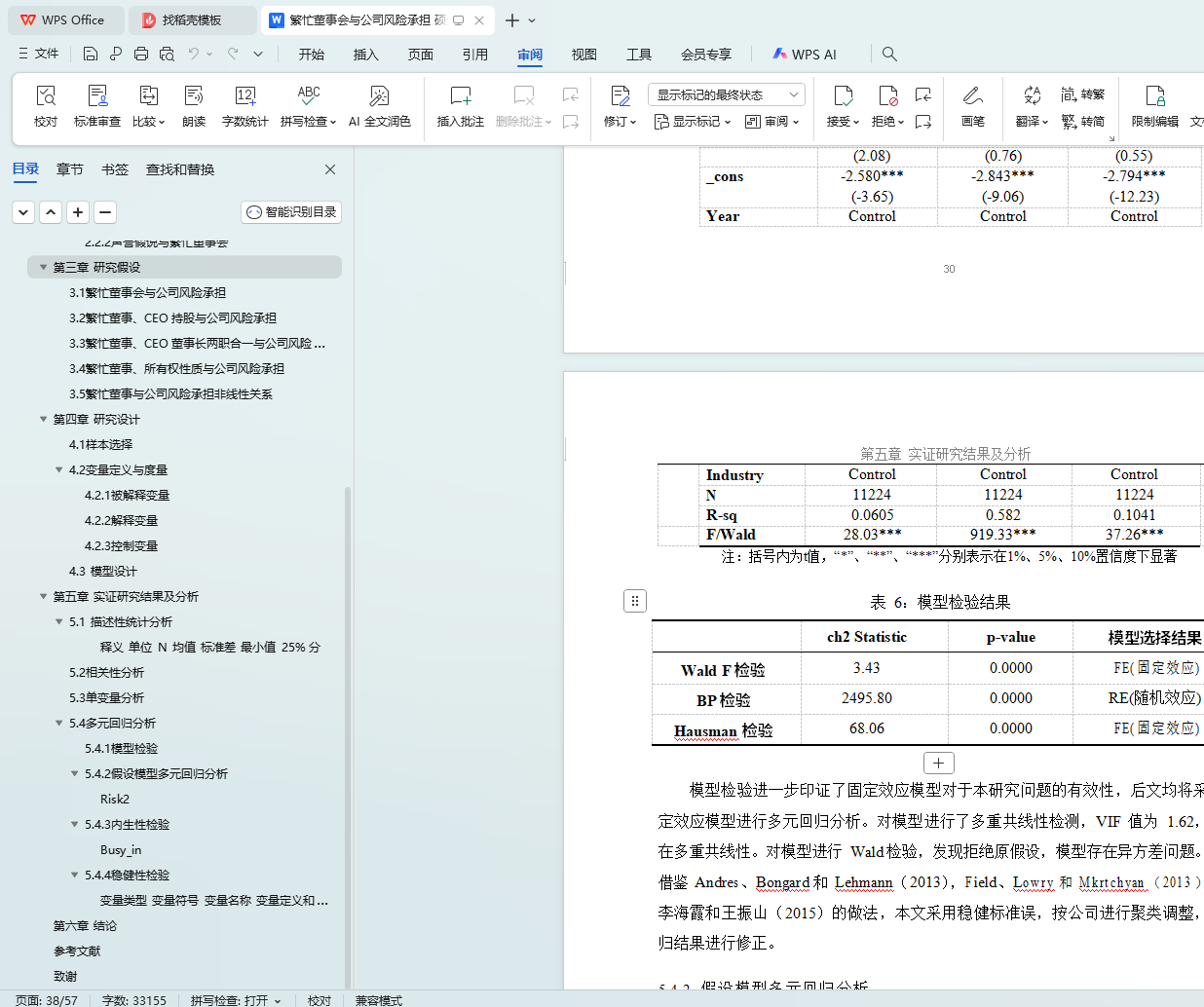

5.4.1 模型检验 29

5.4.2 假设模型多元回归分析 31

5.4.3 内生性检验 39

5.4.4 稳健性检验 41

第六章 结论 44

参考文献 46

致谢 49