摘要

非效率投资是企业的实际投资水平与理想最优水平的偏差。实际投资水平高于最优水平表示公司过度投资,而实际投资低于最优投资水平则是投资不足。无论过度投资还是投资不足,都会导致公司资源的浪费,都会损害投资者和公司的利益。以往的研究表明,非效率投资现象的背后是公司治理问题,具体表现在委托代理、信息不对称等问题。

委托代理问题包括股东与管理层、大股东与中小股东以及债权人与管理层之间的委托代理问题。对于第一种委托代理问题,管理层出于追求自身私人收益、规避风险与私人成本的目的,有利用公司资源进行过度投资或闲置公司资源导致投资不足的动机。对于第二类委托代理问题,大股东更喜欢高的分红和现金流,也往往可以通过董事会和股东大会来控制公司,从而可能会损害中小股东的利益;对于第三种委托代理问题, 因为债权人的利息需要首先支付,对于 NPV>0 的项目,如果不能给股东带来收益,管理层代表着股东的利益也会放弃,造成投资不足;对于收益很高但是风险很大的项目, 股东为了获取高的收益也会投资高风险高收益的项目,造成过度投资。三类委托代理问题是公司非效率投资的主要原因之一。

另外,非效率投资的产生原因还有信息不对称问题。上市公司与投资者之间存在着信息不对称,而信息不对称会影响企业融资的难易程度和融资成本。比如相对于债权人,管理层拥有着更全和更详细的投资信息,债权人因为信息不对称会谨慎投资,造成上市公司面临融资约束,最终造成投资不足。

目前机构投资者管理的资金规模越来越大。相对于散户,机构投资者更加注重长期持有而不是短线交易,也更加积极地参与到公司治理中。对于公司的经营状况,机构投资者往往通过电话、邮件和实地调研等与公司的管理层进行沟通。通过实地调研、电话会议等交流活动,机构投资者能及时了解到公司的经营情况。根据了解到的公司经营情况,机构投资者进行公司价值的判定,并决定投资决策。这也决定着董事会、股东大会中机构投资者的投票,进而参与到公司的治理中。所以机构投资者实地调研、电话会议等不仅仅是对于上市公司的关注,更是起到一种监督作用。

本文从三类委托代理问题和信息不对称问题等视角出发,利用深交所“互动易”平台构建机构投资者关注度指标,并根据 2013-2014 年中国深交所上市公司的数据,实证研究了中国上市公司机构投资者关注度对公司非效率投资的影响。本文先研究了机构投资者关注度对公司非效率投资的影响。因为产权属性对于上市公司投资效率会有不同的影响,所以按照产权属性对上市公司进行分类,分别研究不同产权属性下机构

投资者关注度对公司过度投资、投资不足的影响,最后研究了在机构投资者持股的情况下,机构投资者关注度是否增强了机构投资者持股对公司过度投资、投资不足的影响。

实证结果显示,机构投资者的关注度会抑制公司的非效率投资。对于国企,投资者关注度会减弱公司的过度投资,但对于公司的投资不足没有显著的影响;对于民企,投资者关注度对于投资不足有抑制的作用,但是对于过度投资没有显著影响。这与之前的理论都符合。在机构投资者持股的情况下,投资者关注度会增强机构投资者持股对于国企上市公司过度投资和投资不足的抑制作用。但是对于民营企业来说,投资者关注度会没有显著地增强机构投资者持股对于国企上市公司过度投资和投资不足的抑制作用。

关键词:机构投资者关注度,深交所互动易,非效率投资,公司治理

The Impact of Institutional Investors Attention on Company's Inefficient Investment

Guo Qilin (Finance) Directed by Prof. Wei Cen

ABSTRACT

The inefficiency investment is the deviation of the actual investment level and the ideal optimal level of the enterprise. The actual level of investment is higher than the optimal level is overinvestment, while the actual investment is lower than the optimal level is under investment. Whether overinvestment or underinvestment are all insufficient, they will lead to a waste of company resources and will harm the interests of investors and the company. Previous studies show that the phenomenon of inefficient investment is the problem of corporate governance, which including principal-agent and information asymmetry problems. The principal-agent problem involves the shareholders and the management, the big shareholders and the small shareholders, as well as the creditor and the management. For the first principal-agent problem, the manager pursue personal income, avoid risk and private cost to use company resources to over investment or waste company resources to under investment. For the second principal-agent problems, large shareholders prefer high dividend and cash flow, they can control the company by the board and the general meeting of shareholders, which may harm the interests of minority shareholders; for the third principal agency problem, because the interest of creditors need to first pay, for NPV>0 project, if not bring benefits to shareholders, management who represent the interests of shareholders will give up, resulting in under investment; for high gain but risky project, shareholders who want to obtain high returns will be invest these projects, resulting in excessive investment. The three principal-

agent problems are one of the main reasons for inefficient investment.

In addition, information asymmetry problem also lead to inefficient investment. There is information asymmetry between listing Corporation and investors, and the information asymmetry will affect the difficulty and cost of financing. For example, with respect to creditors, the management has a more comprehensive and more detailed investment information, the creditors will be more cautious because of information asymmetry of, resulting in a listing Corporation facing financing constraints, resulting in under investment.

At present, the scale of the institutional investors are more and more big. Compared to general investors, institutional investors pay more attention to long-term holdings rather than

short-term trading, but also more actively involved in corporate governance. For the company's operating conditions, institutional investors often communication with the company's management by telephone, mail, and field research and. Through field research, conference call and other activities, institutional investors can timely understand the company's operating conditions. According to the understanding of the company's business situation, institutional investors determine the value of the company, and decide investment decision. This also determines the board of directors, the shareholders of the general assembly of institutional investors to vote, and then participate in the company's governance. So institutional investors field research, telephone conference and so on are not only for the listing Corporation's attention, but also a supervisory role.

Based on three kinds of principal-agent problems and asymmetric information the problem, I build institutional investors’ attention index in the perspective of by Shenzhen Stock Exchange interactive “easy platform”. I do an empirical study of Chinese listed companies investment institutions focus on inefficiency investment according to 2013-2014 China Shenzhen Stock Exchange listed company data. Firstly, this paper studies the influence of institutional investors' attention on the inefficient investment of the company. Because property for listed companies will have different effects, so property rights of Listed Companies in accordance with the classification, I study effects of different property rights institutional investors’ attention degree of overinvestment and underinvestment. Finally, the paper studies under the institutional investors, whether institutional investors’ attention degree can enhance the effect of institutional ownership on corporate’s overinvestment and underinvestment.

The empirical results show that institutional investors' attention will restrain the company's inefficient investment. For state-owned enterprises, institutional investors' attention will weaken overinvestment, but not for underinvestment; for private enterprises, institutional investors' attention will weaken underinvestment, but has no significant effect on overinvestment. These are in line with previous theories. In the case of institutional ownership, institutional investors' attention will enhance the effect of institutional ownership on listing Corporation’s overinvestment and underinvestment. But for private enterprises, this enhancement is not very significant.

KEY WORDS: Institutional Investors Attention, Easy Interaction of Shenzhen Stock Exchange, Inefficient Investment; Corporate Governance

目录

摘要 I

ABSTRACT III

目录 V

第一章 引言 1

1.1 研究背景 1

1.2 研究目的和意义 2

1.3 研究方法和内容 2

1.4 本文主要创新和贡献 3

第二章 文献综述 5

2.1 委托代理理论 5

2.2 信息不对称理论 5

2.3 企业非效率投资相关研究 6

2.3.1 非效率投资产生机理 6

2.3.2 影响非效率投资的因素 7

2.3.3 非效率投资的衡量模型 9

2.4 机构投资者持股相关研究 10

2.5 机构投资者与非效率投资的关系研究 12

第三章 理论分析和研究假设 13

3.1 机构投资者关注度与非效率投资 13

3.2 机构投资者关注度、产权属性与非效率投资 13

3.3 机构投资者关注度、机构投资者持股与非效率投资 13

第四章 研究设计 15

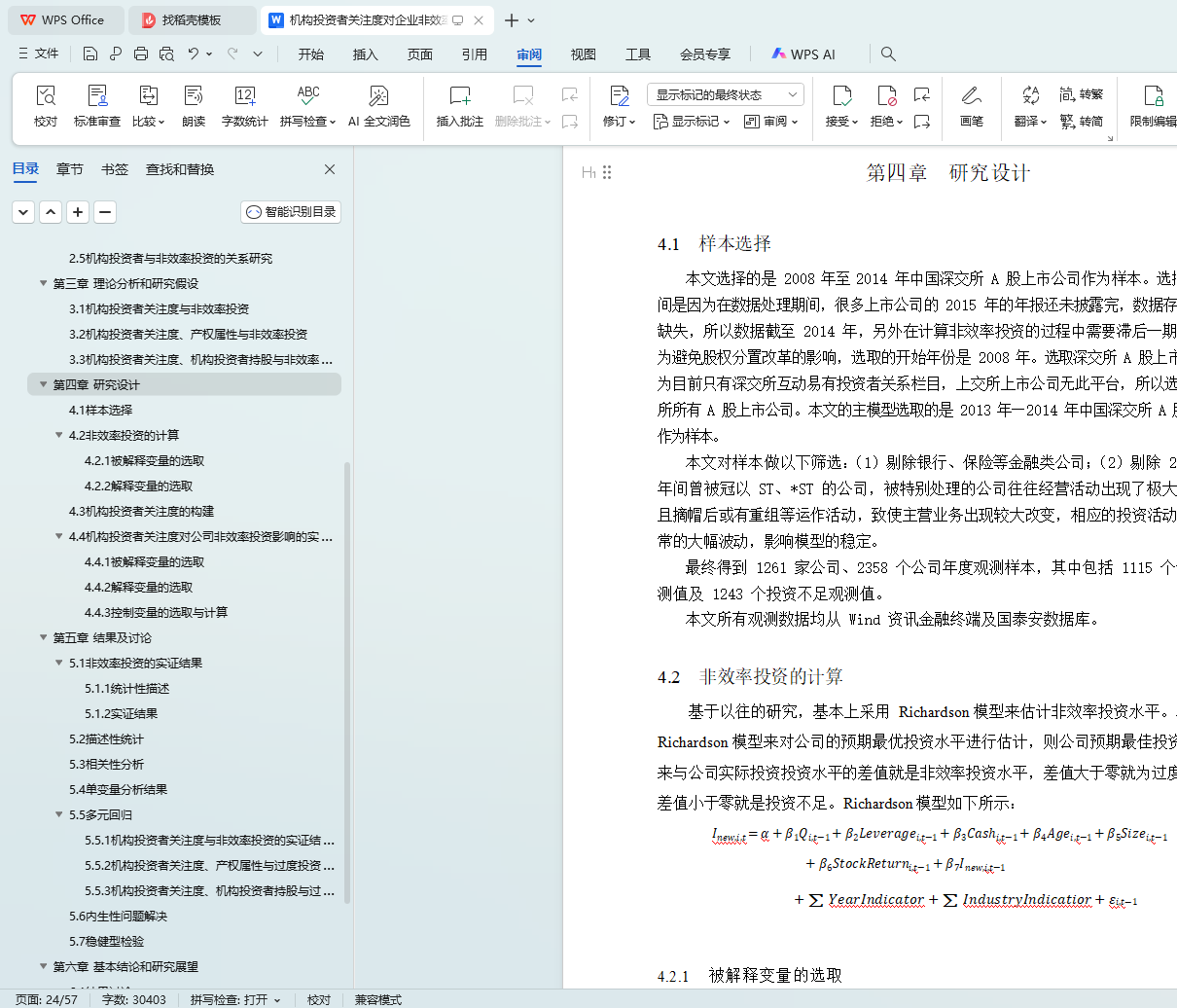

4.1 样本选择 15

4.2 非效率投资的计算 15

4.2.1 被解释变量的选取 15

4.2.2 解释变量的选取 16

4.3 机构投资者关注度的构建 19

4.4 机构投资者关注度对公司非效率投资影响的实证模型 19

4.4.1 被解释变量的选取 20

4.4.2 解释变量的选取 20

4.4.3 控制变量的选取与计算 20

第五章 结果及讨论 24

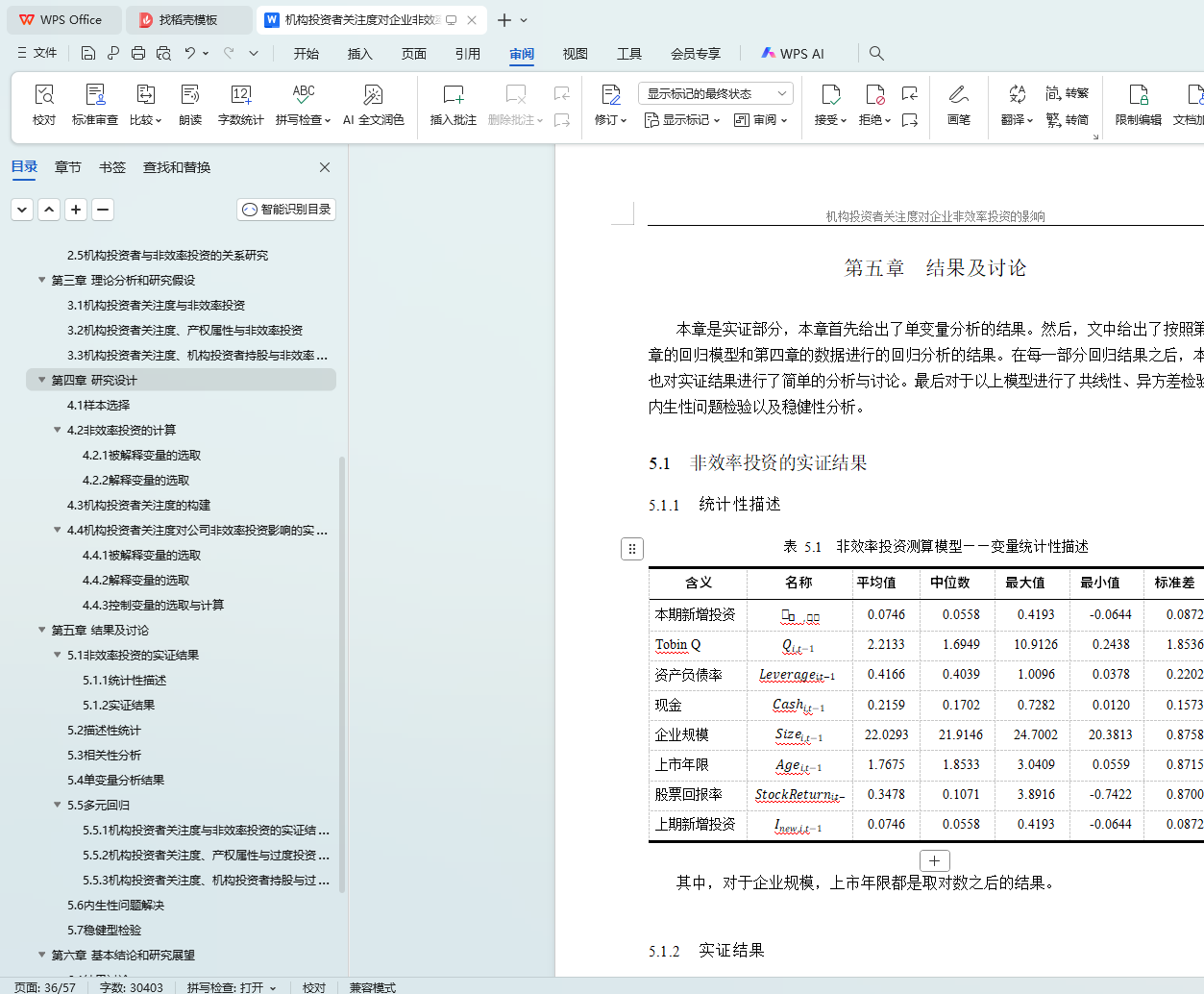

5.1 非效率投资的实证结果 24

5.1.1 统计性描述 24

5.1.2 实证结果 24

5.2 描述性统计 25

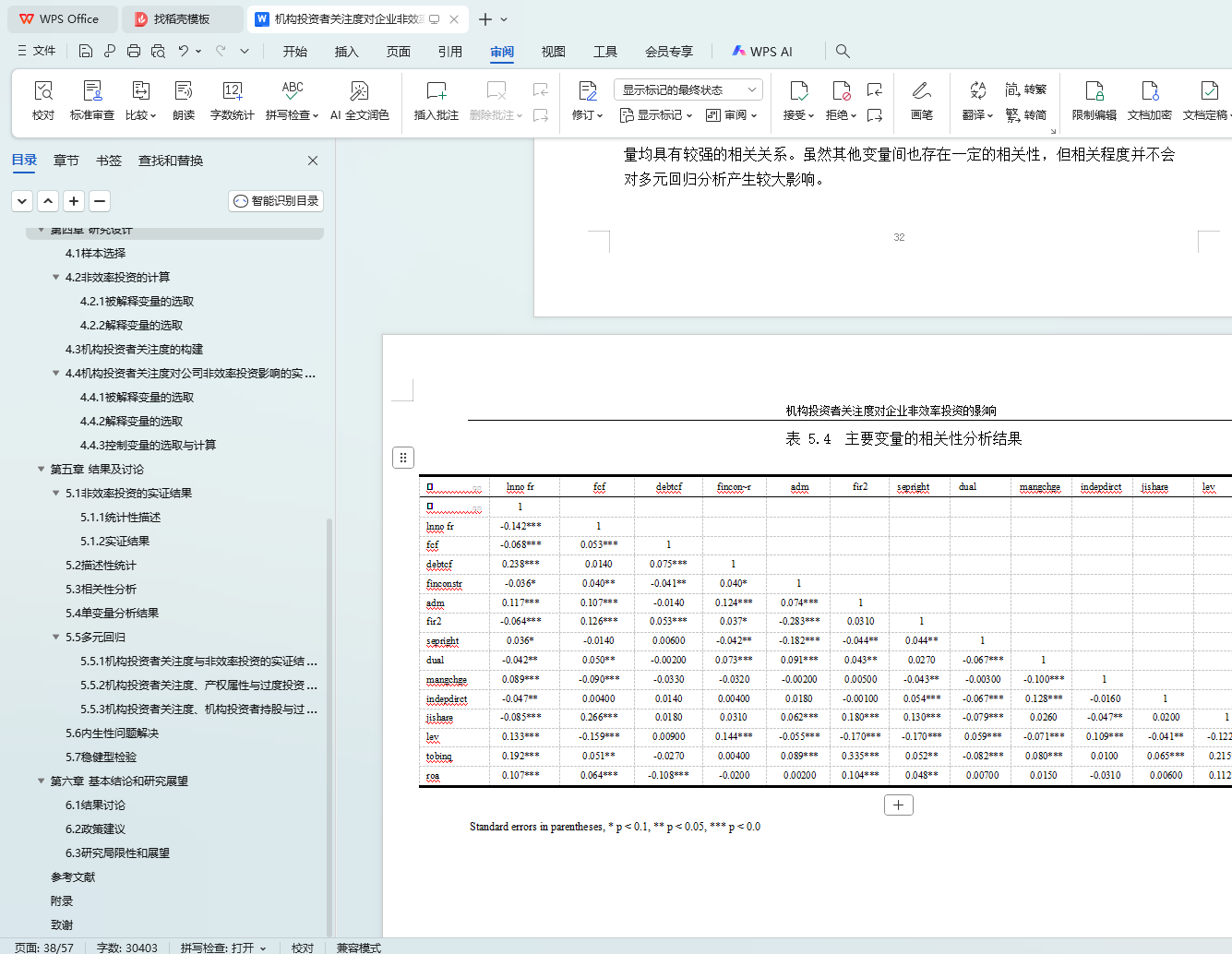

5.3 相关性分析 26

5.4 单变量分析结果 29

5.5 多元回归 29

5.5.1 机构投资者关注度与非效率投资的实证结果 29

5.5.2 机构投资者关注度、产权属性与过度投资、投资者不足的实证结果 33

5.5.3 机构投资者关注度、机构投资者持股与过度投资、投资者不足的实证结果 34

5.6 内生性问题解决 36

5.7 稳健型检验 37

第六章 基本结论和研究展望 39

6.1 结果讨论 39

6.2 政策建议 39

6.3 研究局限性和展望 40

参考文献 41

附录 43

致谢 46