我国房地产上市公司融资结构与公司绩效的实证研究

【摘要】

房地产作为我国国民经济的关键性基础产业,其健康稳定的运行对我国经济的发展具有有效的促进作用。而且,健康合理地进行房地产市场的扩张,将有利于我国社会的和谐发展。我国房地产行业自2009年开始,行业资产负债率不断提高,2016年已是攀升至78.3%。资产负债率过高,财务风险加大,显然对房地产业的健康发展是不利的。而企业融资结构的合理优化有助于其融资成本的减少,从而能够增强房地产企业进行风险抵御的能力,进而增加房地产企业的绩效水平。对房地产企业的融资结构与公司绩效的关系研究,能够很大程度上促进企业对其关系的深入认识,进一步结合自身的发展现状,合理改善自身融资结构,提高其绩效水平,进而促进房地产市场的健康稳定发展,并联动其他产业的健康发展,促进我国经济的健康稳定的持续发展。

本文的研究对象为我国房地产业,首先梳理了国内外知名学者关于融资结构同公司绩效之间影响关系的研究文献,并对融资结构优化的相关理论进行阐述。然后,从理论上分析了我国房地产业的融资结构对公司绩效的影响关系。接着,对我国目前的房地产业的融资结构现状以及绩效水平现状进行了详细分析。再对我国A股市场上市的房地产公司进行了实证分析,选取了涵盖公司偿债能力、发展能力、经营能力以及盈利能力共19个指标进行因子分析,提取公因子创建公司绩效得分,并建立回归模型对其融资结构和公司绩效得分进行分析,回归结果表明我国房地产上市公司的资产负债率对公司绩效得分具有显著的负向影响,也就是说资产负债率越高的房地产上市公司,其公司绩效水平越低。对此,本文提出了相关建议:(1)降低资产负债率;(2)创新融资方式,拓展融资渠道;(3)强化企业风险意识。

【关键词】房地产上市公司;融资结构;企业绩效

【ABSTRACT】

The real estate industry is an important basic industry in the national economy. The stable development of the real estate industry can effectively promote the prosperity and development of the national economy. At the same time, the healthy and rational expansion of the real estate market plays an important role in promoting social harmony and improving people’s living standards. Since 2009, the average asset-liability ratio of China’s real estate development companies has continued to rise, reaching a high of 78.3% by 2016. According to statistics, most of the debt funds of real estate development companies come from banks, which is obviously not conducive to the sustained and healthy development of the real estate industry. The optimization of the financing structure can reduce the financing costs to a great extent, thereby increasing the ability of real estate companies to resist risks and improving the company's operating performance. By studying the financing structure and corporate performance of real estate companies, companies can help them better understand the relationship between the two, and choose their own financing structure and improve their performance according to the actual development status of the company, promote the development of the real estate industry and drive other industries.

This article selects China's real estate industry as the research object. First, it reviews domestic and foreign scholars' research on the relationship between financing structure and company's operating performance, and conducts a theoretical analysis on the financing structure of the real estate industry. Then the paper analyzes the current situation of corporate performance and financing structure in China's real estate industry. Then, through empirical analysis, factor analysis is mainly used to create a corporate performance score, and then a regression model is established to study the correlation between the financing structure and corporate performance. It is concluded that there is a negative correlation between asset-liability ratio and corporate performance of real estate companies. At the end of the article, based on the results of the study, it puts forward its own proposals for the current situation and hopes to provide its own strength for improving the financing structure of China's real estate companies.

【Key words】real estate listed company, financing structure, corporate performance

目录

【摘要】

【ABSTRACT】

1 绪 论

1.1 研究背景

1.2 研究意义

1.2.1理论意义

1.2.2实践意义

1.3研究方法及内容

1.3.1研究方法

1.3.2研究内容

2 文献综述及相关理论

2.1文献综述

2.1.1国外文献综述

2.1.2国内研究综述

2.2资本结构优化理论

2.2.1传统资本结构理论

2.2.2现代资本结构理论

2.2.3新资本结构理论

2.3融资结构与企业绩效关系的理论分析

3 我国房地产行业现状分析

3.1我国房地产行业概况

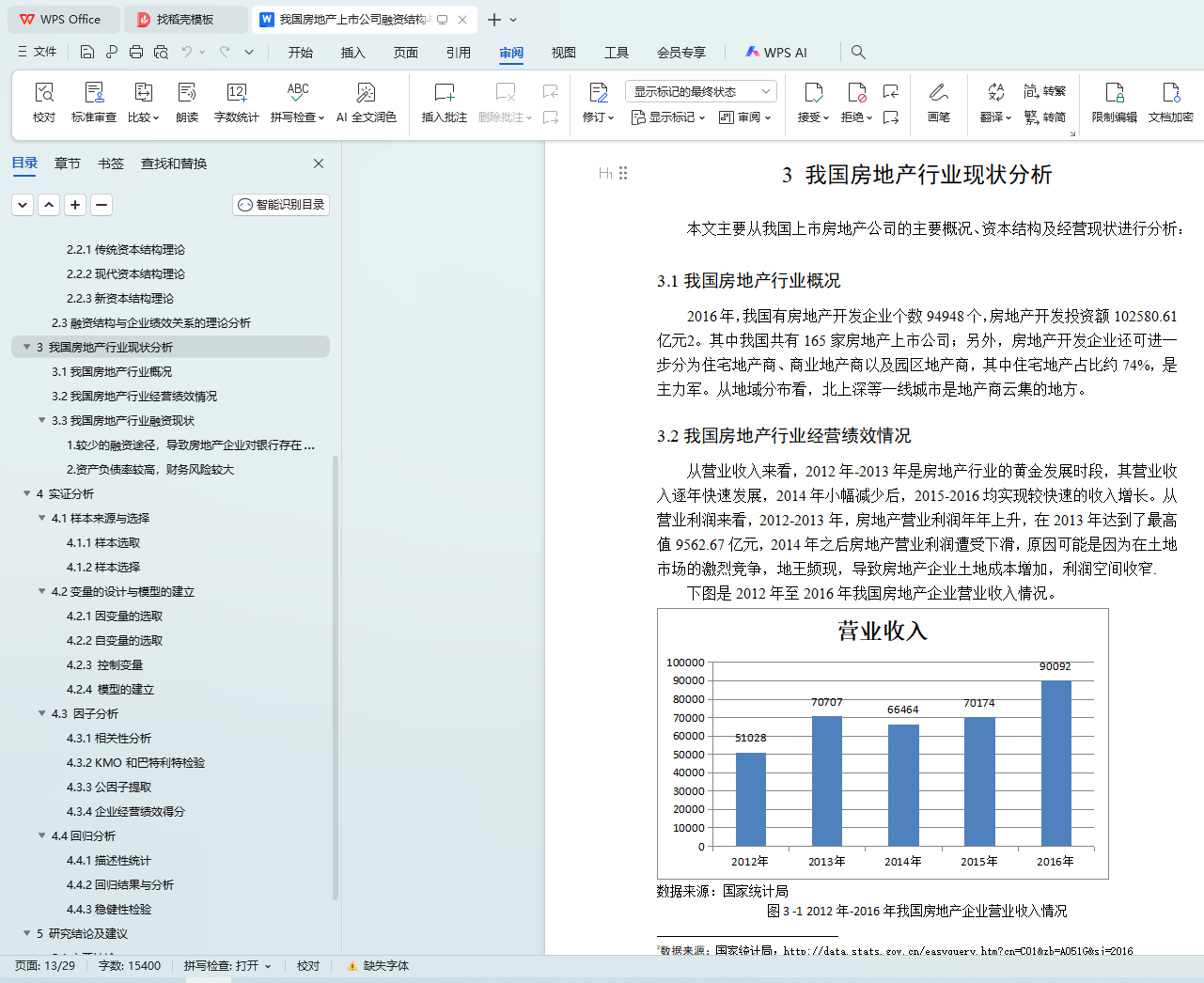

3.2我国房地产行业经营绩效情况

3.3我国房地产行业融资现状

1.较少的融资途径,导致房地产企业对银行存在较大的依赖性

2.资产负债率较高,财务风险较大

4 实证分析

4.1样本来源与选择

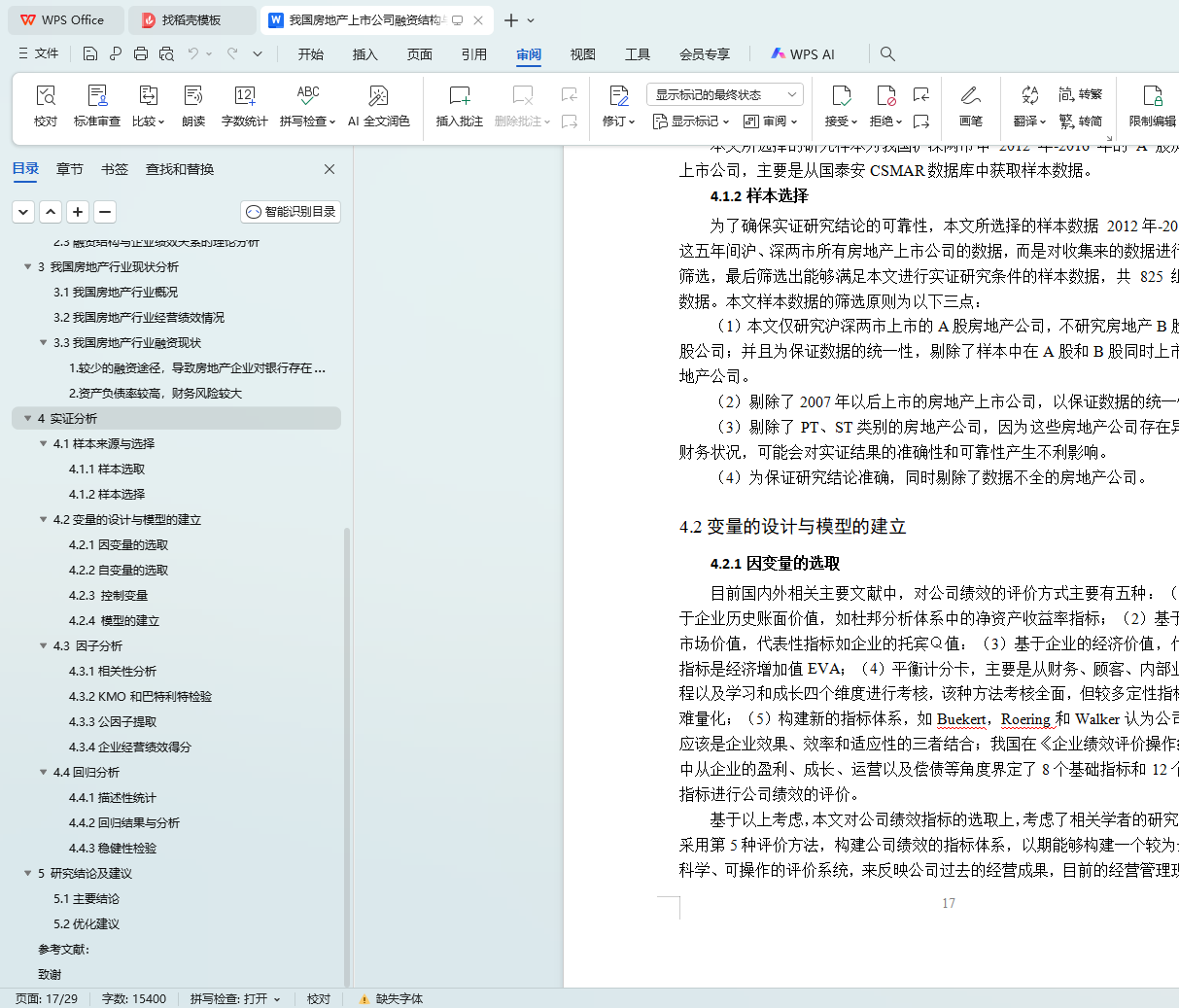

4.1.1样本选取

4.1.2样本选择

4.2变量的设计与模型的建立

4.2.1因变量的选取

4.2.2自变量的选取

4.2.3 控制变量

4.2.4 模型的建立

4.3 因子分析

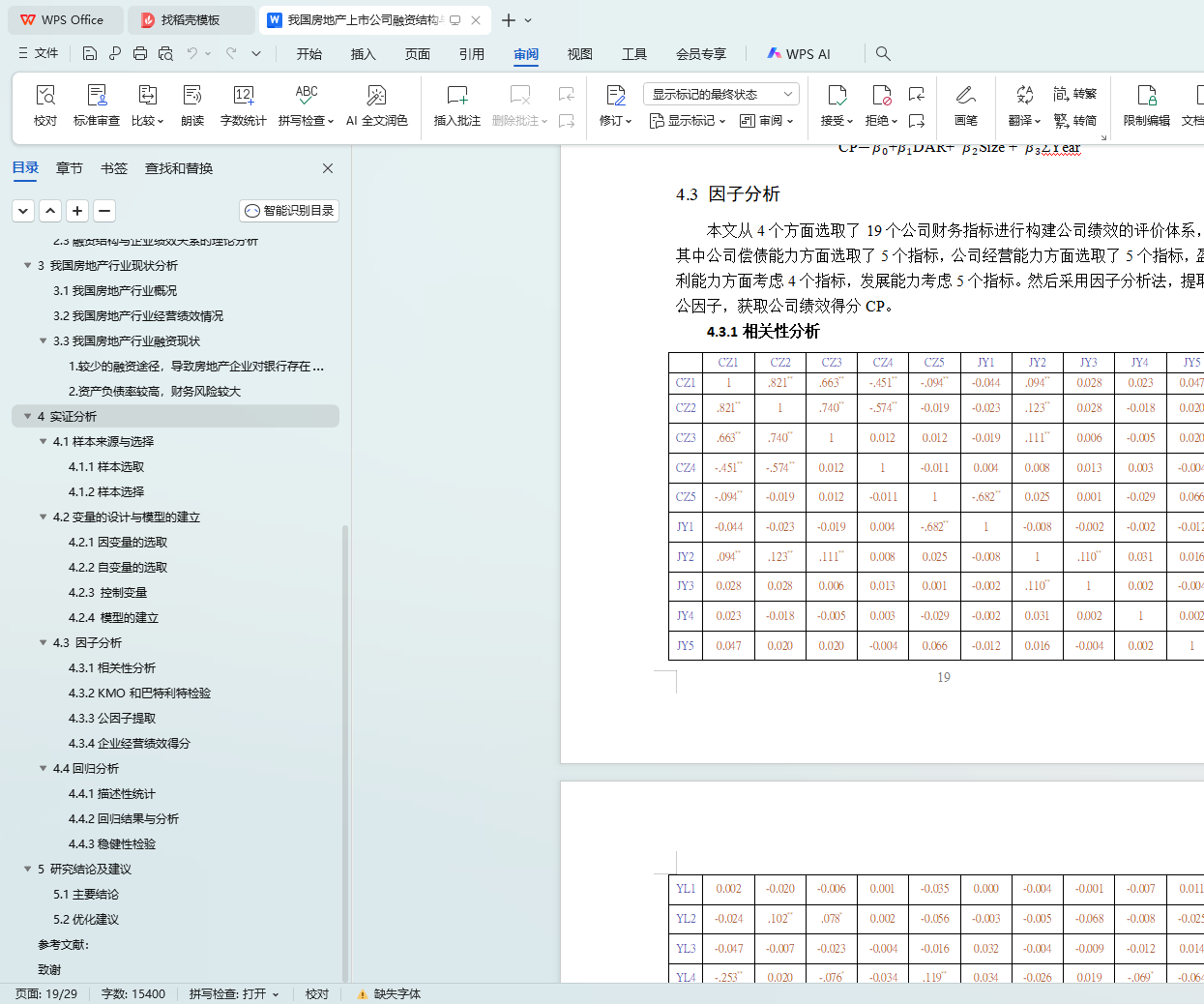

4.3.1相关性分析

4.3.2 KMO和巴特利特检验

4.3.3公因子提取

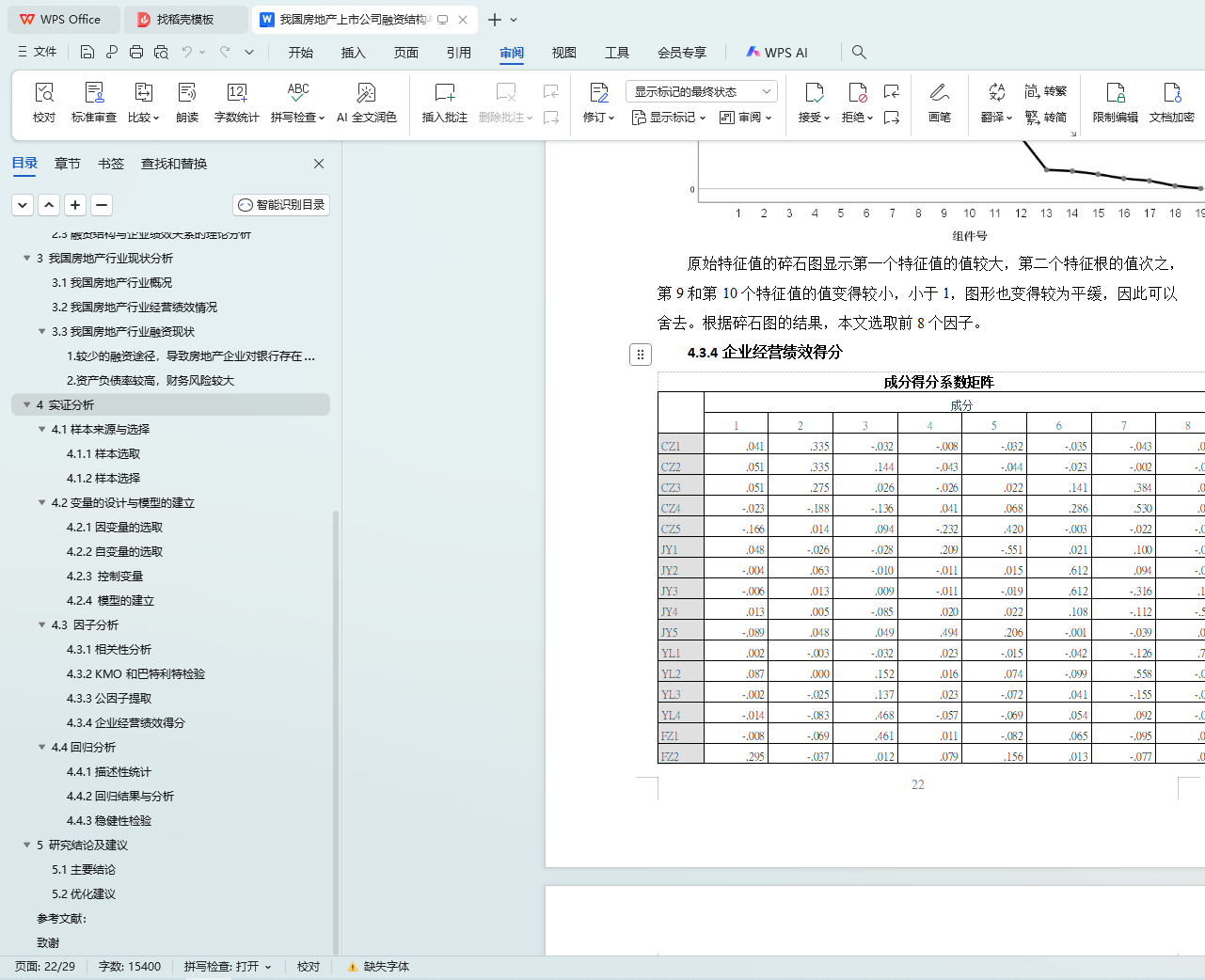

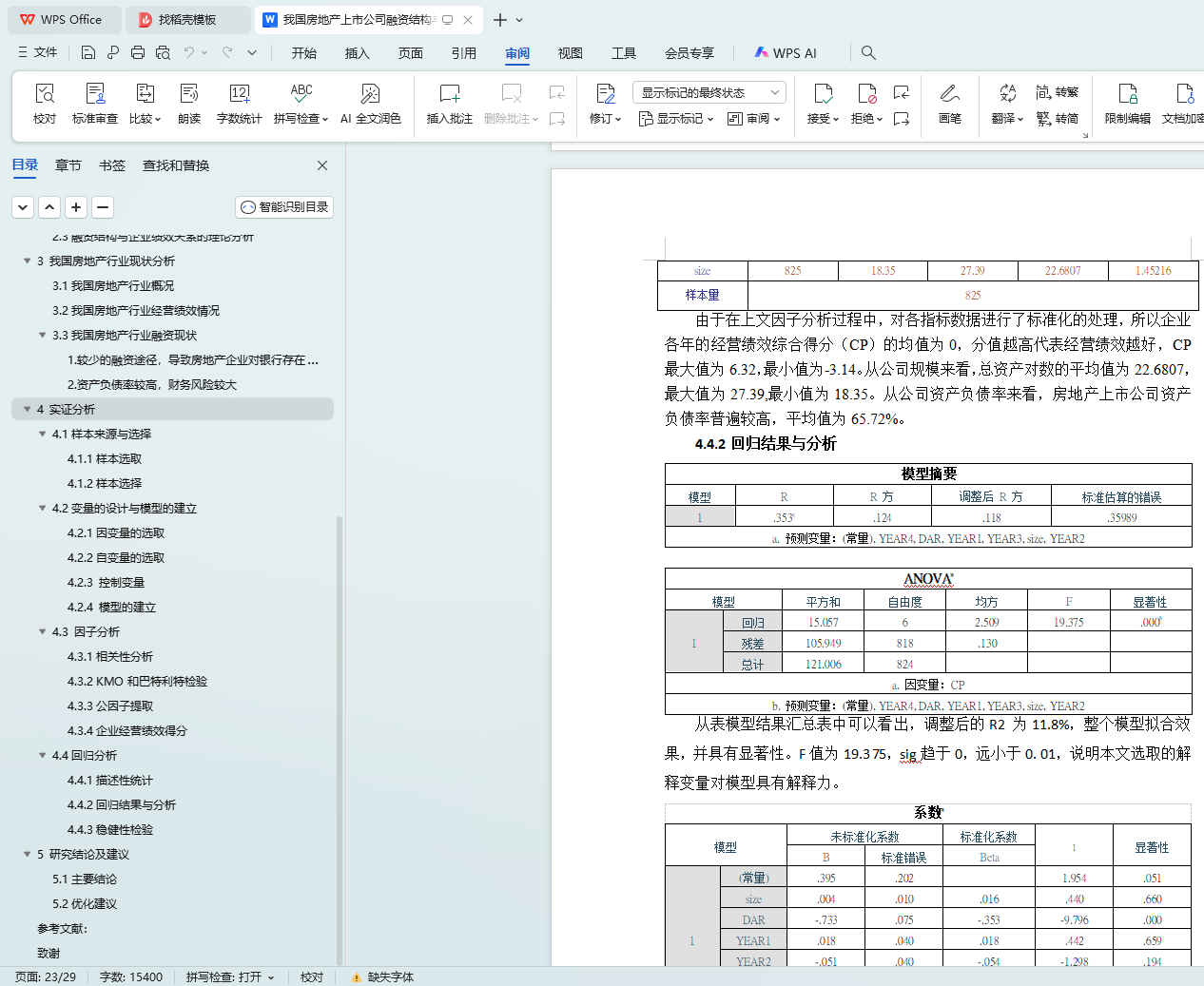

4.3.4企业经营绩效得分

4.4回归分析

4.4.1描述性统计

4.4.2回归结果与分析

4.4.3稳健性检验

5 研究结论及建议

5.1主要结论

5.2优化建议

参考文献

致谢