摘要

企业越来越倾向雇佣有财务背景的 CEO,CEO 作为企业首席执行官对投资决策有重要的影响,决定企业的资本配置过程,其财务工作经历的背景能够提高资本配置效率,帮助企业把握有价值的投资机会。基于现实意义,本文深入探究 CEO 财务背景对资本配置效率的影响,并对其影响机制进行了验证和分析。

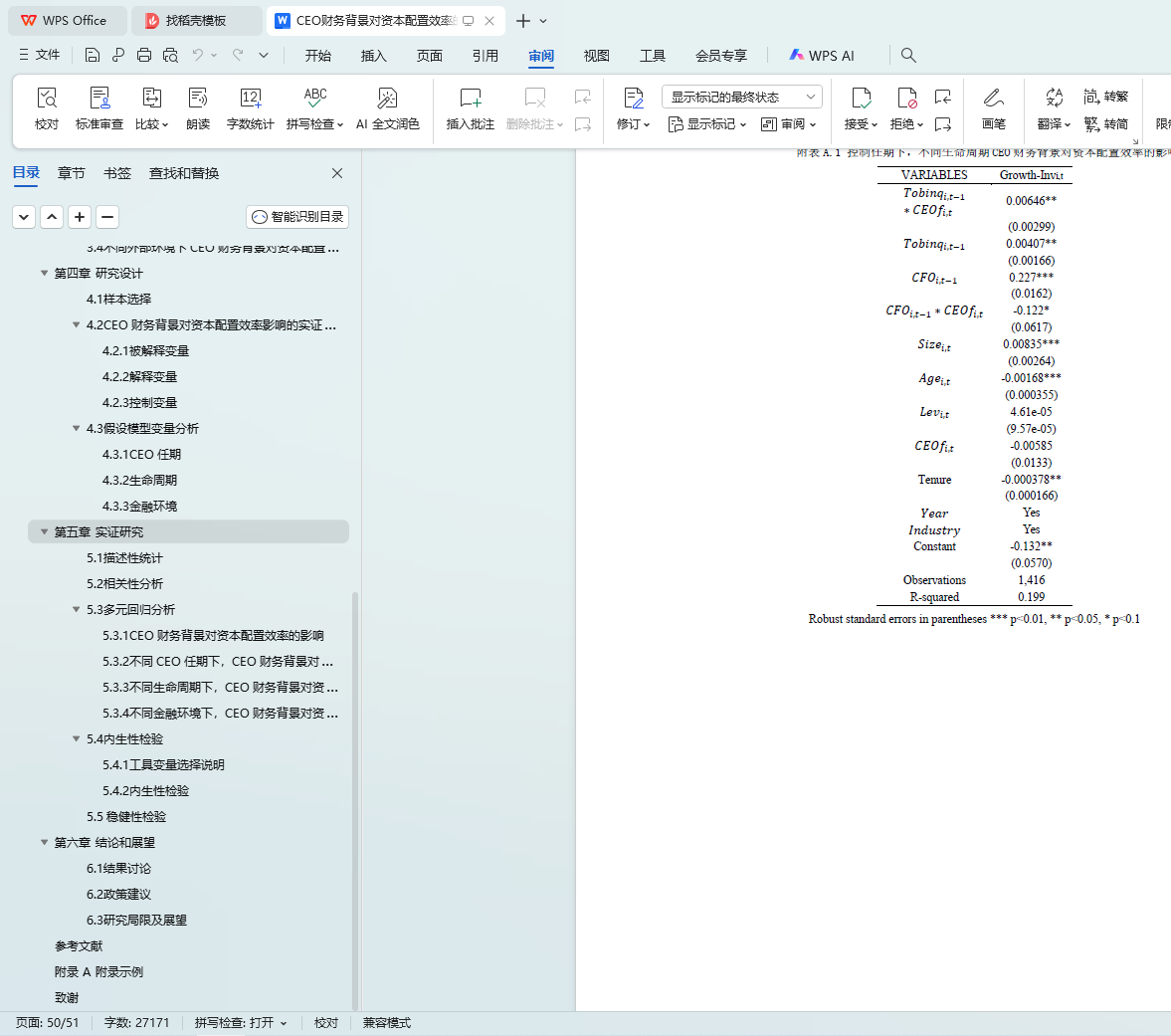

本文采用了 Mclean et al.(2012)的研究方法,利用投资与滞后一期的托宾 Q 的系数来衡量企业对投资机会的敏感程度,系数越大,说明企业对投资机会的反应越灵敏, 越能把握有价值的投资机会。研究结果表明,具有财务背景的 CEO 能够显著提高资本配置效率,主要是通过两条传导途径进行传导。一是具有财务背景的 CEO 有更好的识别项目的能力,这是 CEO 个人特征的影响,即对高阶理论的丰富。二是具有财务背景的 CEO 有更强的融资能力,融资成本较低,主要体现在 CEO 善于利用债务等多样化融资方式调整资本结构,善于披露高质量的财务信息,同时注重与银行、投资人等关系的维护。这两条传导途径使得具有财务背景的 CEO 能够更好的识别投资机会,同时其较强的融资能力为投资提供了保障,提高了对资本的利用效率。

为了进一步验证传导机制,本文按照生命周期、CEO 任期进行分组回归,发现成长期、CEO 既有任期较短时期 CEO 财务背景对资本配置效率的影响显著。同时验证了金融危机时期的影响效果。综上,当企业内外部环境比较混乱时,CEO 的财务背景对资本配置效率的影响更显著。

本文研究为企业雇佣有财务背景的 CEO 提供了理论支持,同时也为丰富了高阶理论,为 CEO 任命、高管团队构建及公司治理等提供借鉴意义。

关键词:资本配置效率,CEO 财务背景,CEO 任期,生命周期

CEO Financial Background and Capital Allocation Efficiency

Tingting Luo (Finance) Directed by Wei Cen

ABSTRACT

Companies tend to hire CEOs with financial backgrounds. CEO has an important impact on investment decisions and determine the capital allocation process of the company. The background of their financial work experience can improve the efficiency of capital allocation and help companies to grasp valuable investment opportunities. Based on the practical significance, the paper explores the influence of CEO financial background on capital allocation efficiency, and analyzes its mechanism.

In this paper, we use the research method of Mclean et al. (2012), using the sensitivity of investment to lagged Tobin Q to measure the capital allocation efficiency. The larger the coefficient, the more sensitive the response of the firm to the investment opportunity, the more to grasp the valuable investment opportunities. The results show that CEOs with financial background can significantly improve capital allocation efficiency, mainly through two transmission mechanism. First, a CEO with financial background has a better ability to identify the project, which is the impact of the CEO's personal characteristics, that is, rich in Upper Echelons Theory. Second, the financial background of the CEO has a stronger financing capacity, mainly reflected in the good use of debt and other diversified financing way to adjust the capital structure, good disclosure of high-quality financial information, while focusing on the relationship with banks, investors. By the two mechanisms, CEO with financial background can significantly improve the capital allocation efficiency.

In order to further verify the transmission mechanism, the paper follows the life cycle, the CEO tenure. It is found that the financial background of CEO has a significant impact on the capital allocation efficiency when the firm in growth-stage and the CEO in short tenure. While verifying the impact of the financial crisis. To sum up, when the internal and external environment is chaotic, the CEO's financial background on the efficiency of capital allocation is more significant.

This paper provides theoretical support for hiring a CEO with financial background and also enriches Upper Echelons Theory and provides suggestions for the appointment of CEO and corporate governance.

KEY WORDS: Capital Allocation Efficiency, CEO Financial Background,CEO

Tenure, Life Cycle

目录

摘要 I

ABSTRACT II

目录 III

第一章 引言 1

1.1 研究背景 1

1.2 研究目的及意义 2

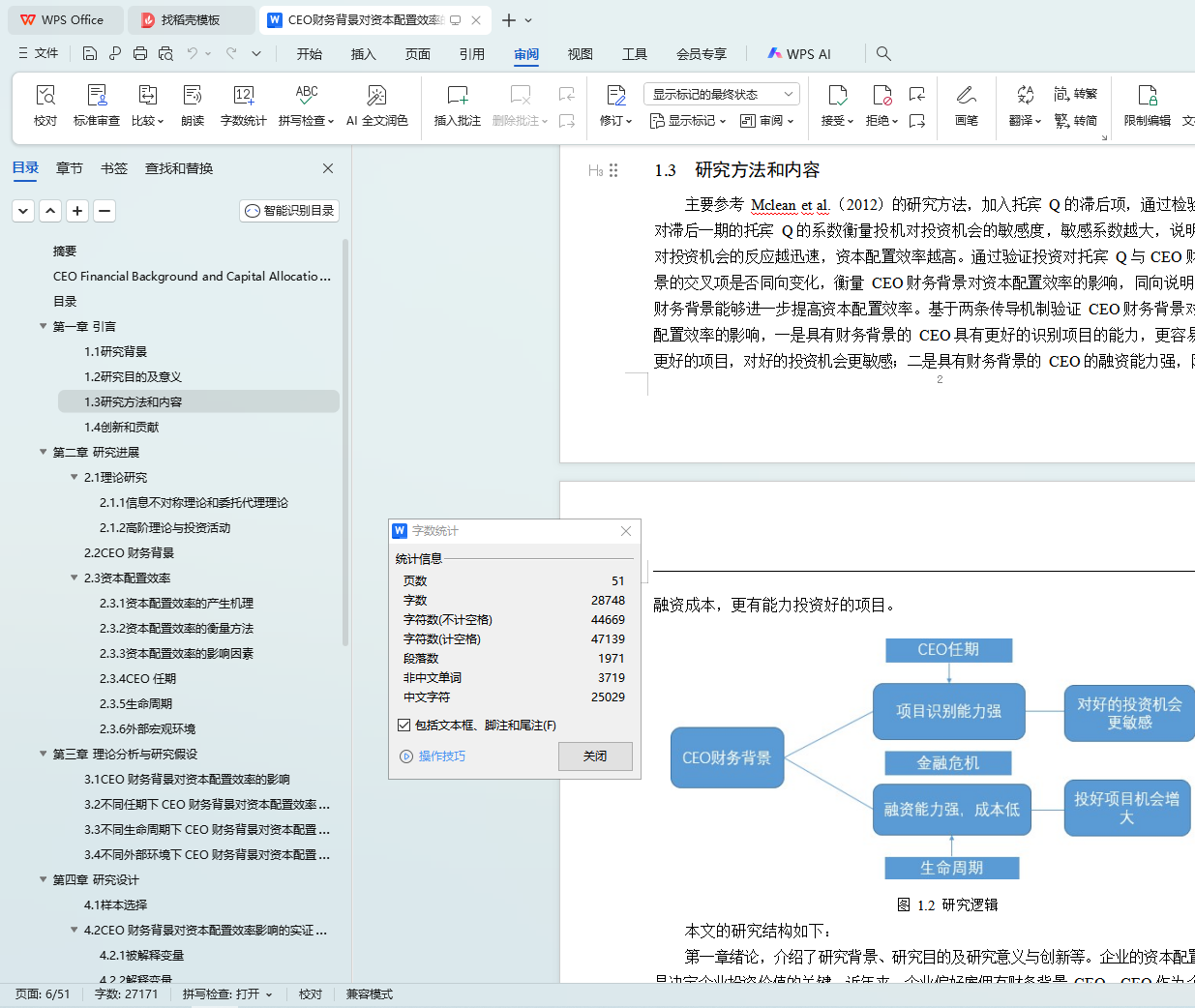

1.3 研究方法和内容 2

1.4 创新和贡献 4

第二章 研究进展 5

2.1 理论研究 5

2.1.1 信息不对称理论和委托代理理论 5

2.1.2 高阶理论与投资活动 5

2.2 CEO 财务背景 7

2.3 资本配置效率 8

2.3.1 资本配置效率的产生机理 8

2.3.2 资本配置效率的衡量方法 8

2.3.3 资本配置效率的影响因素 9

2.3.4 CEO 任期 10

2.3.5 生命周期 11

2.3.6 外部宏观环境 12

第三章 理论分析与研究假设 13

3.1 CEO 财务背景对资本配置效率的影响 13

3.2 不同任期下 CEO 财务背景对资本配置效率的影响 13

3.3 不同生命周期下 CEO 财务背景对资本配置效率的影响 14

3.4 不同外部环境下 CEO 财务背景对资本配置效率的影响 14

第四章 研究设计 16

4.1 样本选择 16

4.2 CEO 财务背景对资本配置效率影响的实证模型 16

4.2.1 被解释变量 17

III

4.2.2 解释变量 17

4.2.3 控制变量 17

4.3 假设模型变量分析 18

4.3.1 CEO 任期 18

4.3.2 生命周期 19

4.3.3 金融环境 19

第五章 实证研究 20

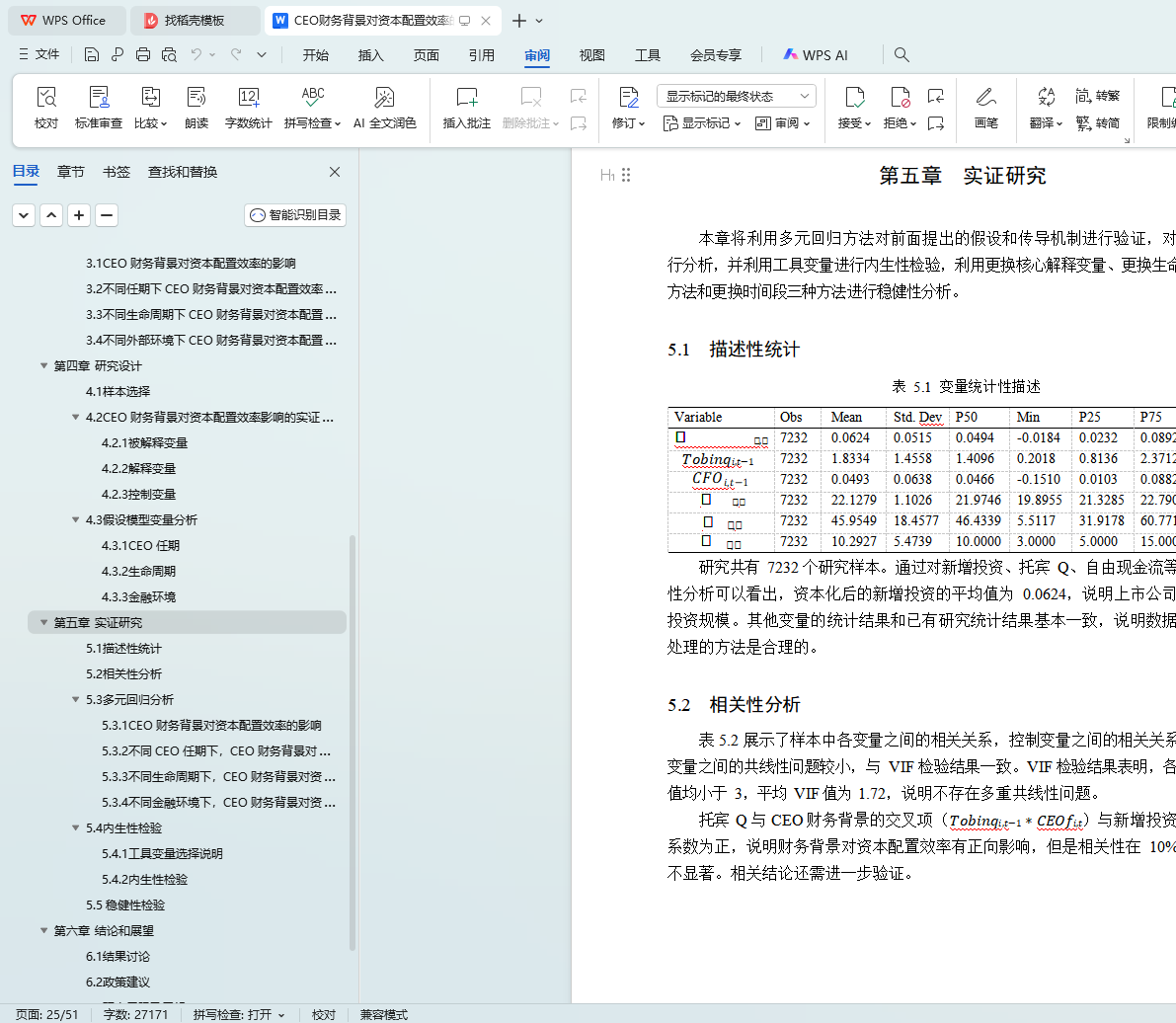

5.1 描述性统计 20

5.2 相关性分析 20

5.3 多元回归分析 22

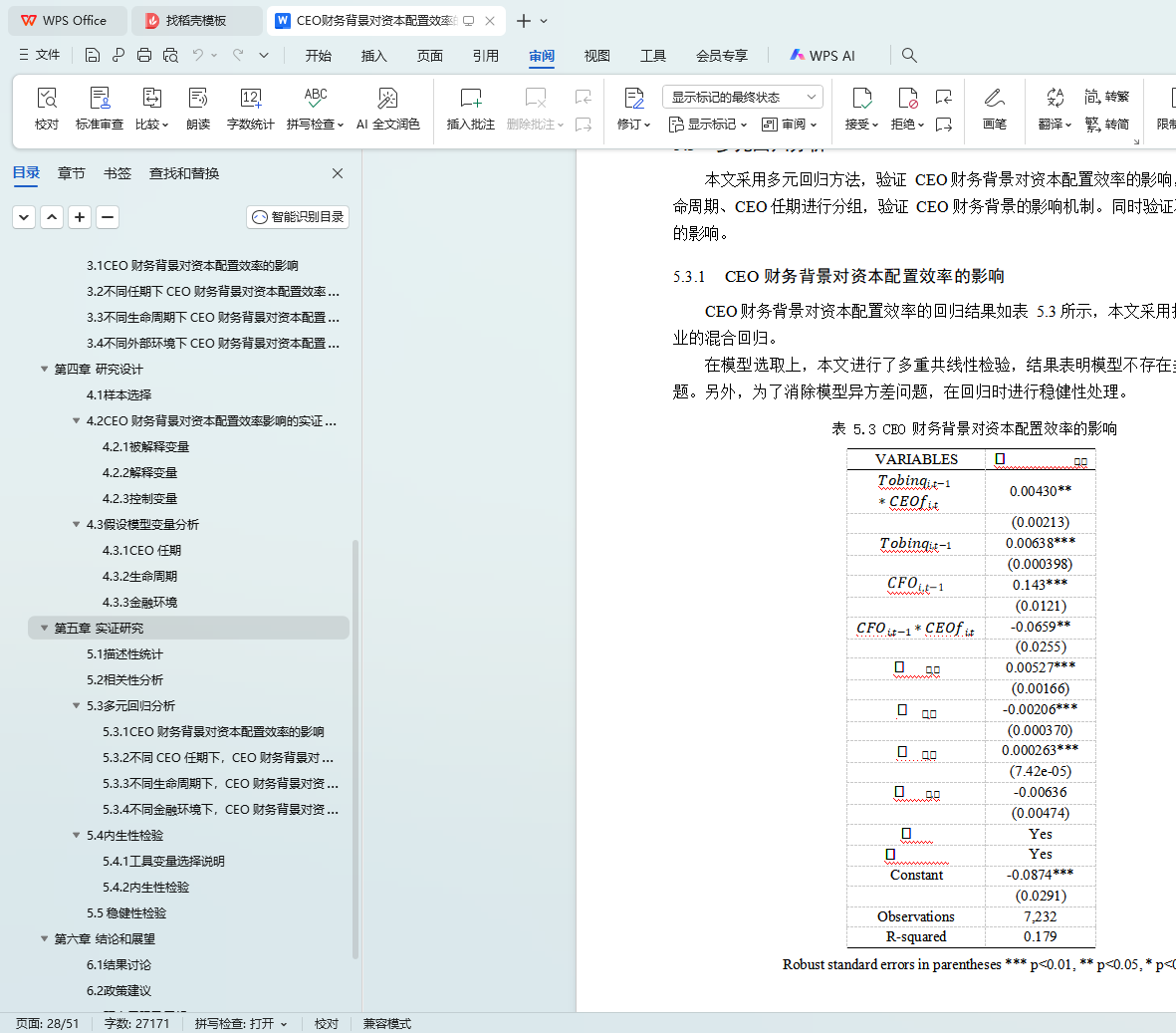

5.3.1 CEO 财务背景对资本配置效率的影响 22

5.3.2 不同 CEO 任期下,CEO 财务背景对资本配置效率的影响 24

5.3.3 不同生命周期下,CEO 财务背景对资本配置效率的影响 25

5.3.4 不同金融环境下,CEO 财务背景对资本配置效率的影响 27

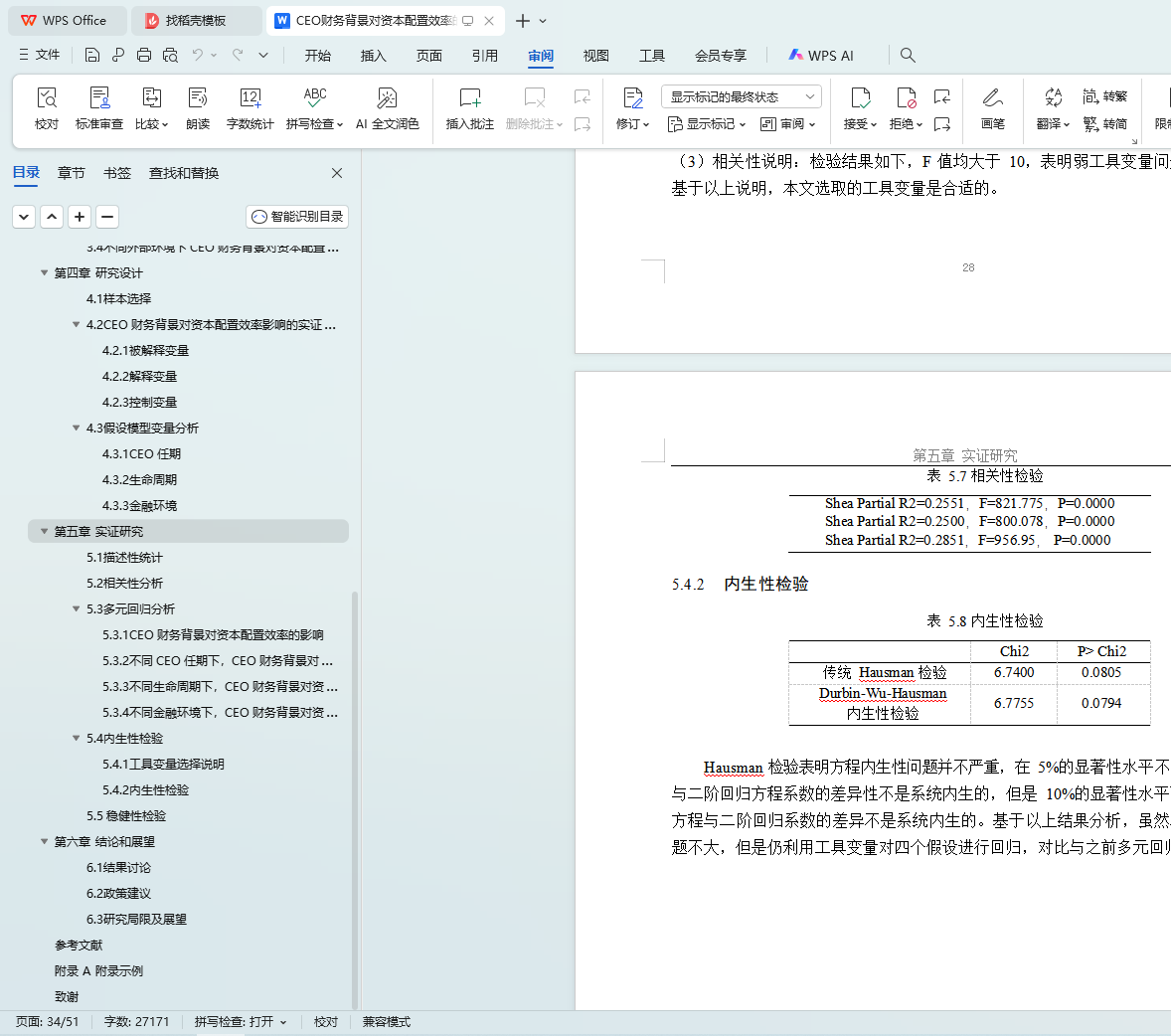

5.4 内生性检验 28

5.4.1 工具变量选择说明 28

5.4.2 内生性检验 29

5.5 稳健性检验 34

第六章 结论和展望 38

参考文献 40

附录 A 附录示例 43

致谢 44