基于ARIMA模型对上证指数的预测

【摘要】

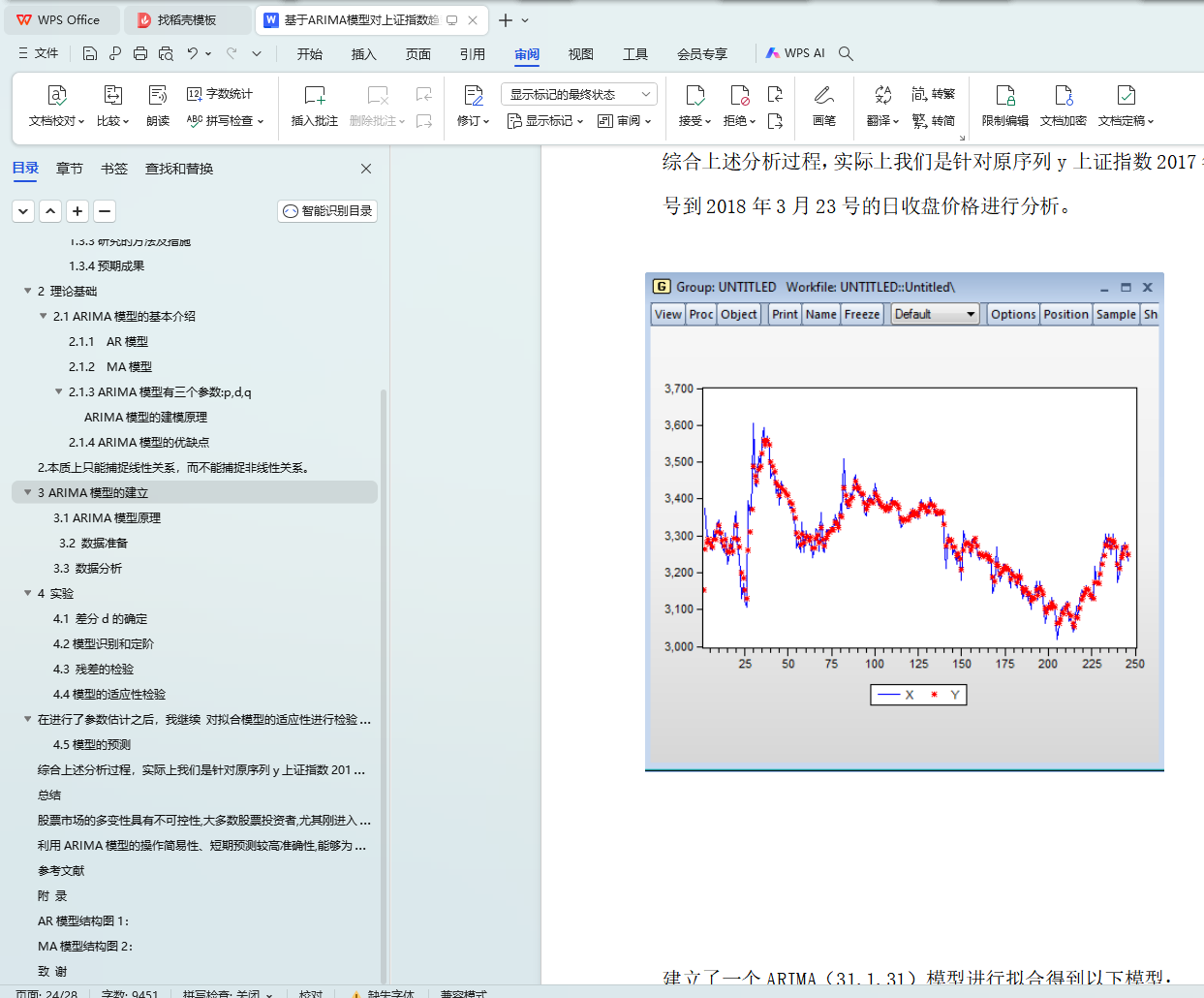

本文利用EView 7建立了上海证券交易所指数的ARIMA模型,并对其股价进行了初步预测。差分运算具有强大的确定性信息提取能力,许多非平稳序列差分后会显示出平稳序列的性质。这时我们称这个非平稳序列为差分平稳序列。对差分平稳序列可以使用ARIMA模型。股票价格变化一般都是不平稳的,所以我们就应该对其进行差分处理,不能直接使用ARMA模型,ARIMA模型基于原始序列是否平稳以及回归过程的不同部分,包括移动平均过程(MA)、自回归过程(ARA)、自回归移动平均过程(ARMA)和ARIMA过程。

由于股票价格变动中存在诸多不确定因素,各因素之间的关系复杂,理论上难以对股票价格进行彻底的预测。然而股市是一个运动的、特殊的系统,它必然也存在着特殊的规律

【关键词】 上证综合指数,ARIMA模型,EViews7

Prediction of Shanghai stock index based on ARIMA model

【Abstract】

In this paper, we use EView 7 to establish the ARIMA model of Shanghai stock exchange index, and make a preliminary prediction of its stock price. Differential operation has strong ability of deterministic information extraction, and many non-stationary sequence will show the nature of stationary sequence after difference. We call this nonstationary sequence a differential stationary sequence. The ARIMA model can be used for the differential stationary sequence. The change of stock price is generally not smooth, so we should do differential processing, and we should not use the ARMA model directly. The ARIMA model is based on whether the original sequence is stable and the different parts of the regression process, including the moving average process (MA), the autoregressive process (ARA), the autoregressive moving average process (ARMA) and the ARIMA process.

Because there are many uncertainties in the change of stock prices and the complex relationship between the various factors, it is difficult to predict the stock market price thoroughly in theory. However, the stock market is a sports, special system, and it is bound to have special rules.

【Key Words】 Shanghai composite index, ARIMA model, EViews7

目 录

1 绪 论 6

1.1 研究背景及意义 6

1.2 国内外研究现状 6

1.3 本文的主要内容与组织结构 7

1.3.1 本文的主要内容 7

1.3.2 本文的组织结构 7

1.3.4预期成果 7

2 理论基础 8

2.1 ARIMA模型的基本介绍 8

2.1.1 AR模型 8

2.1.2 MA模型 8

2.1.3 ARIMA模型有三个参数:p,d,q 8

2.1.4 ARIMA模型的优缺点 9

3 3 ARIMA模型的建立 9

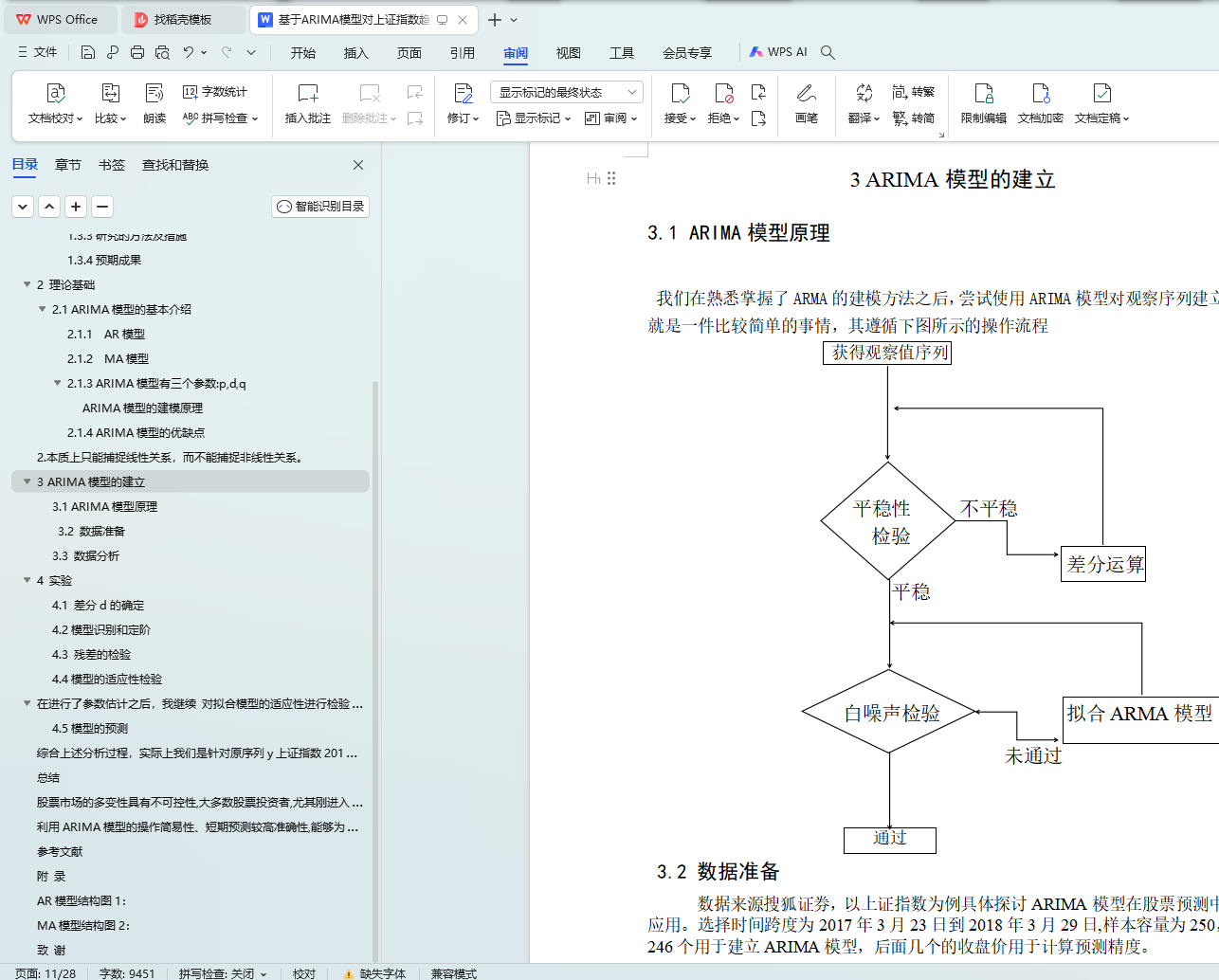

3.1 ARIMA模型原理 9

3.2 数据准备 10

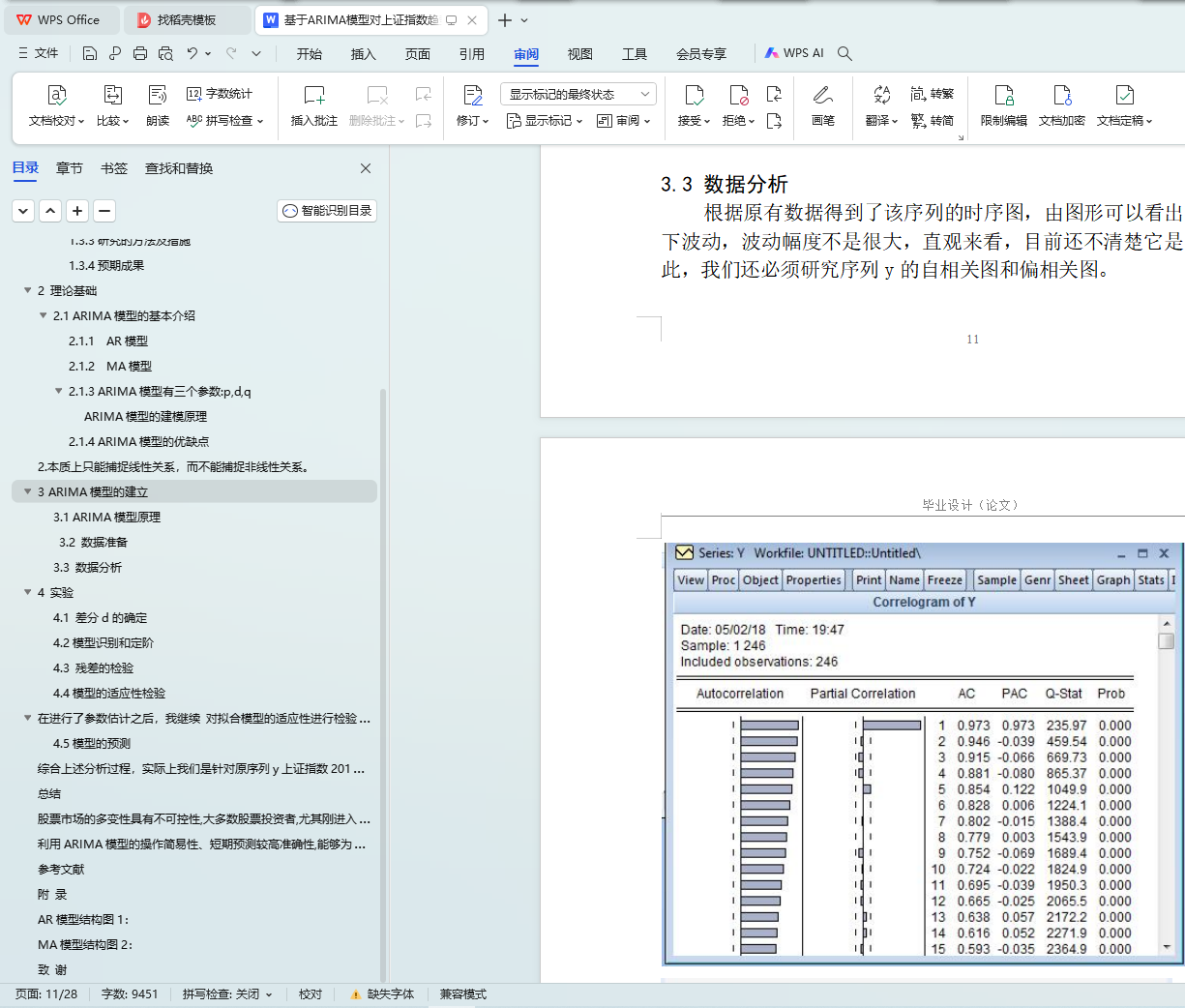

3.3 数据分析 13

4 实验 14

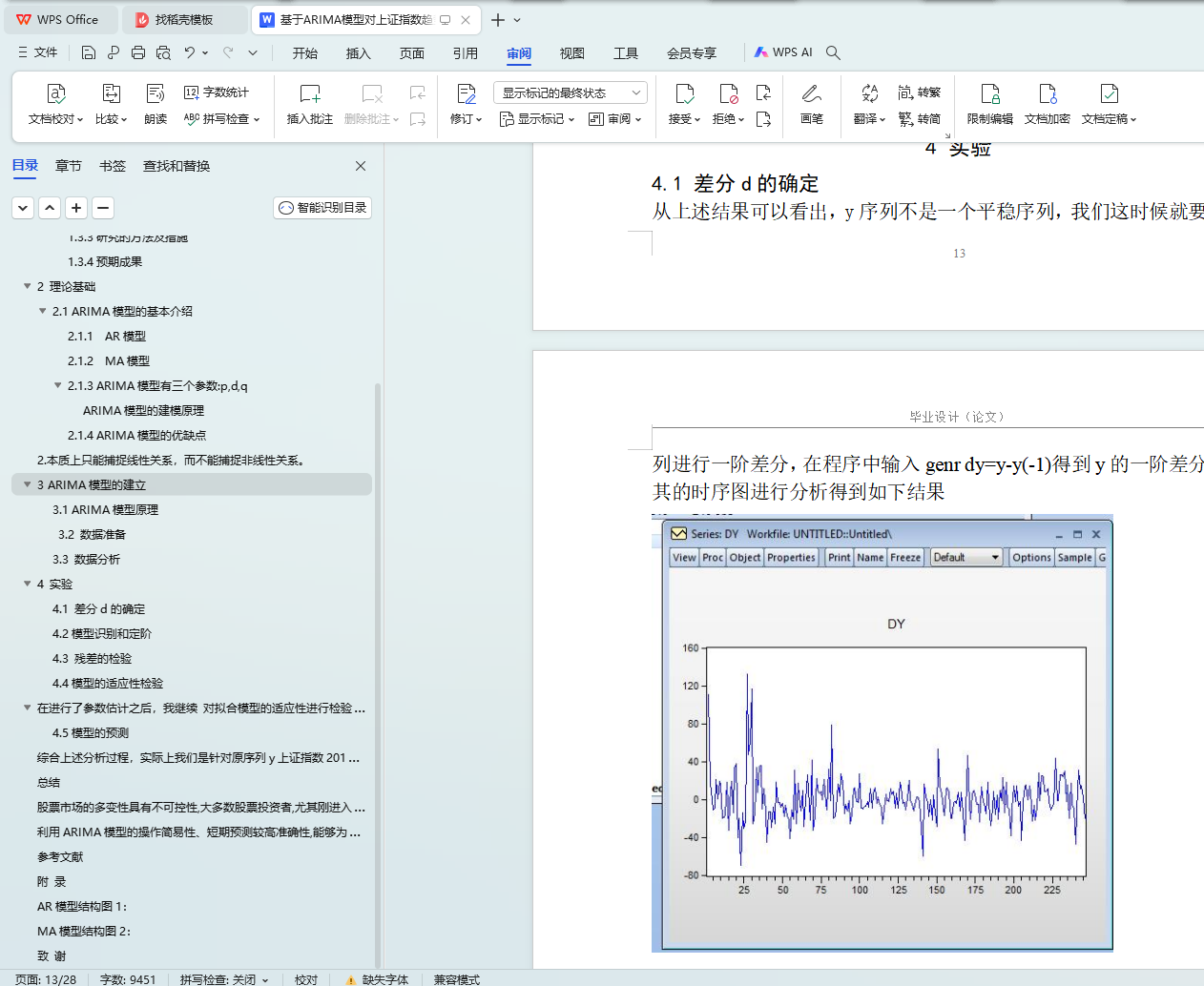

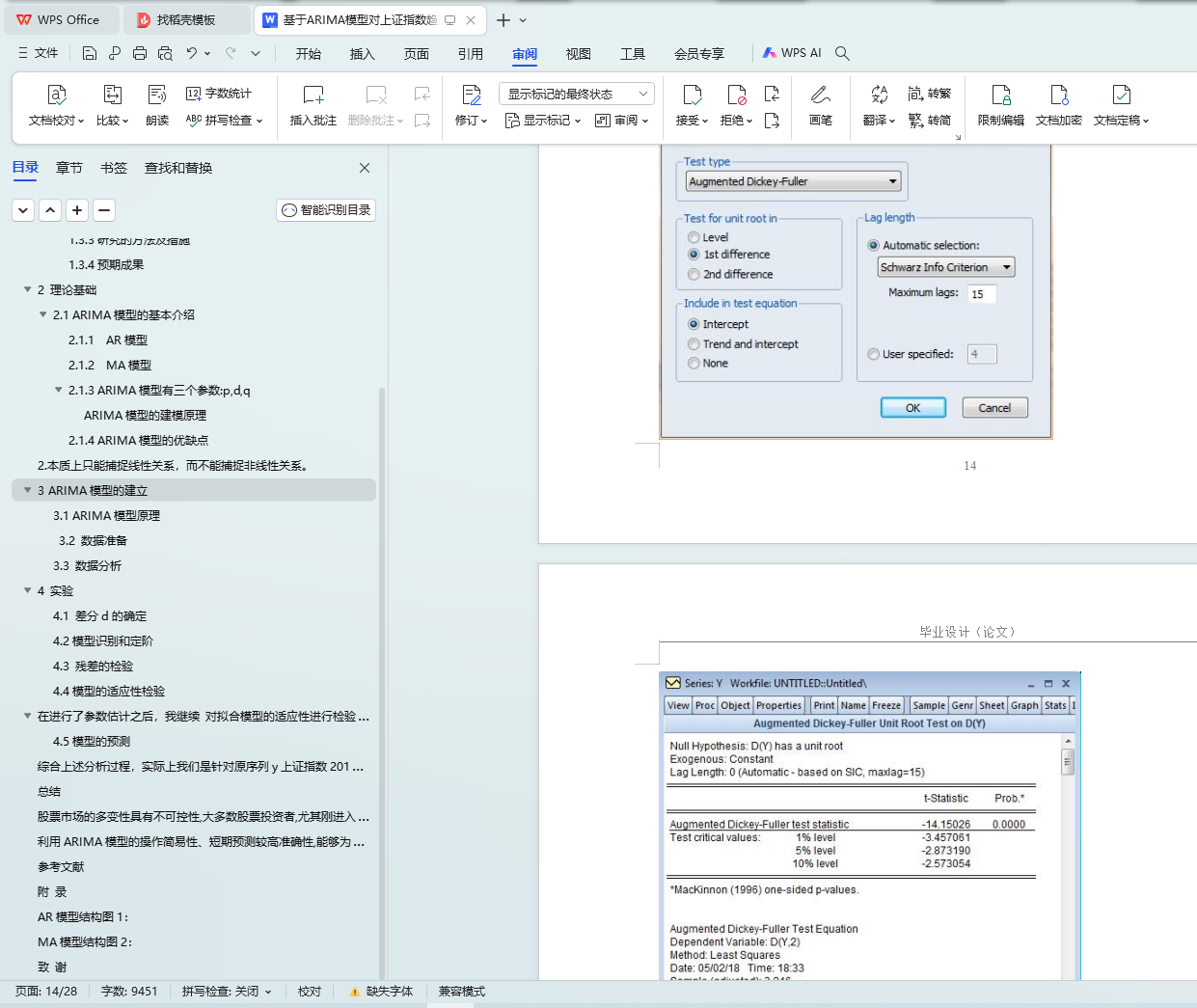

4.1 差分d的确定 16

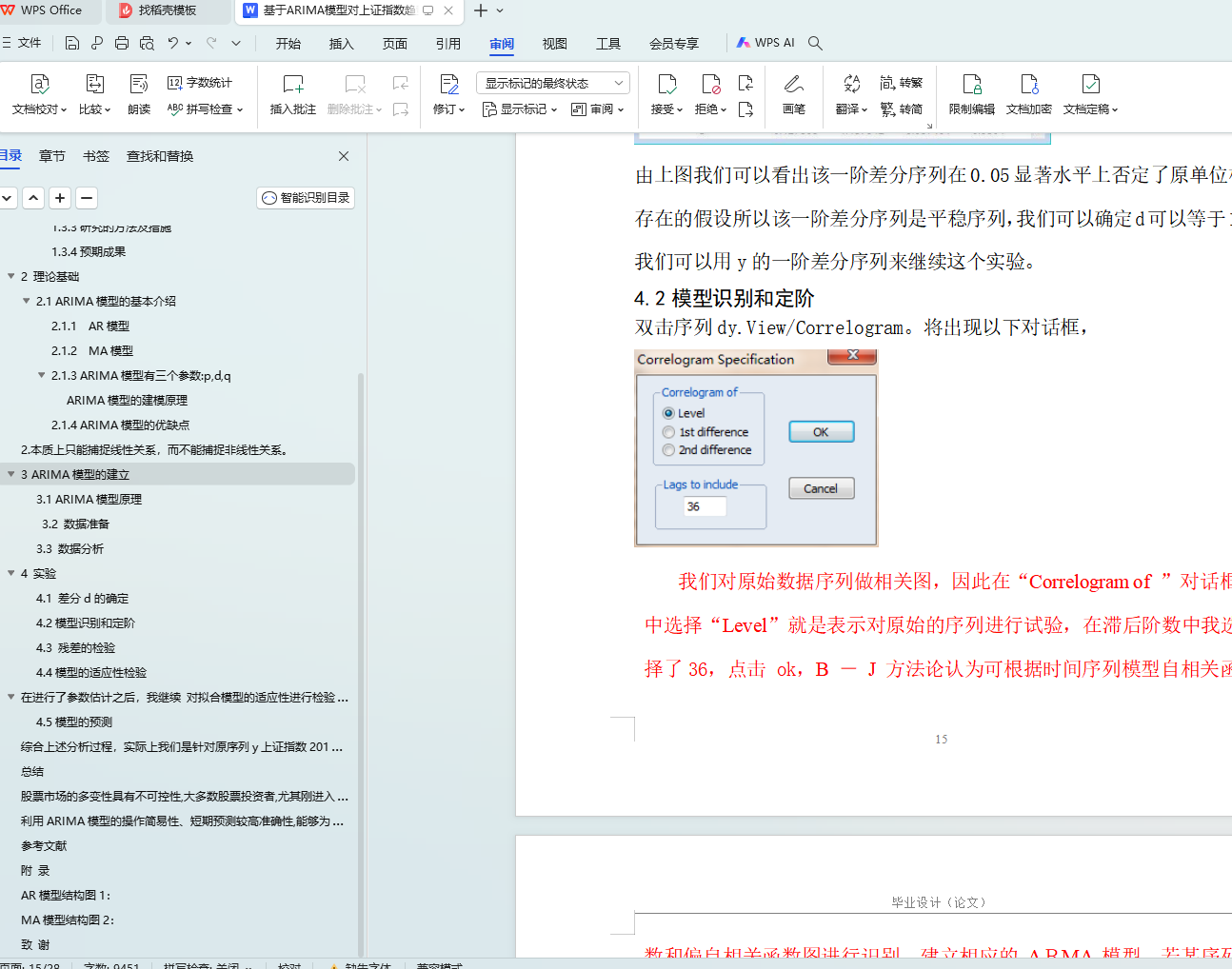

4.2模型识别和定阶 18

4.3残差的检验 20

4.4模型的适应性检验 23

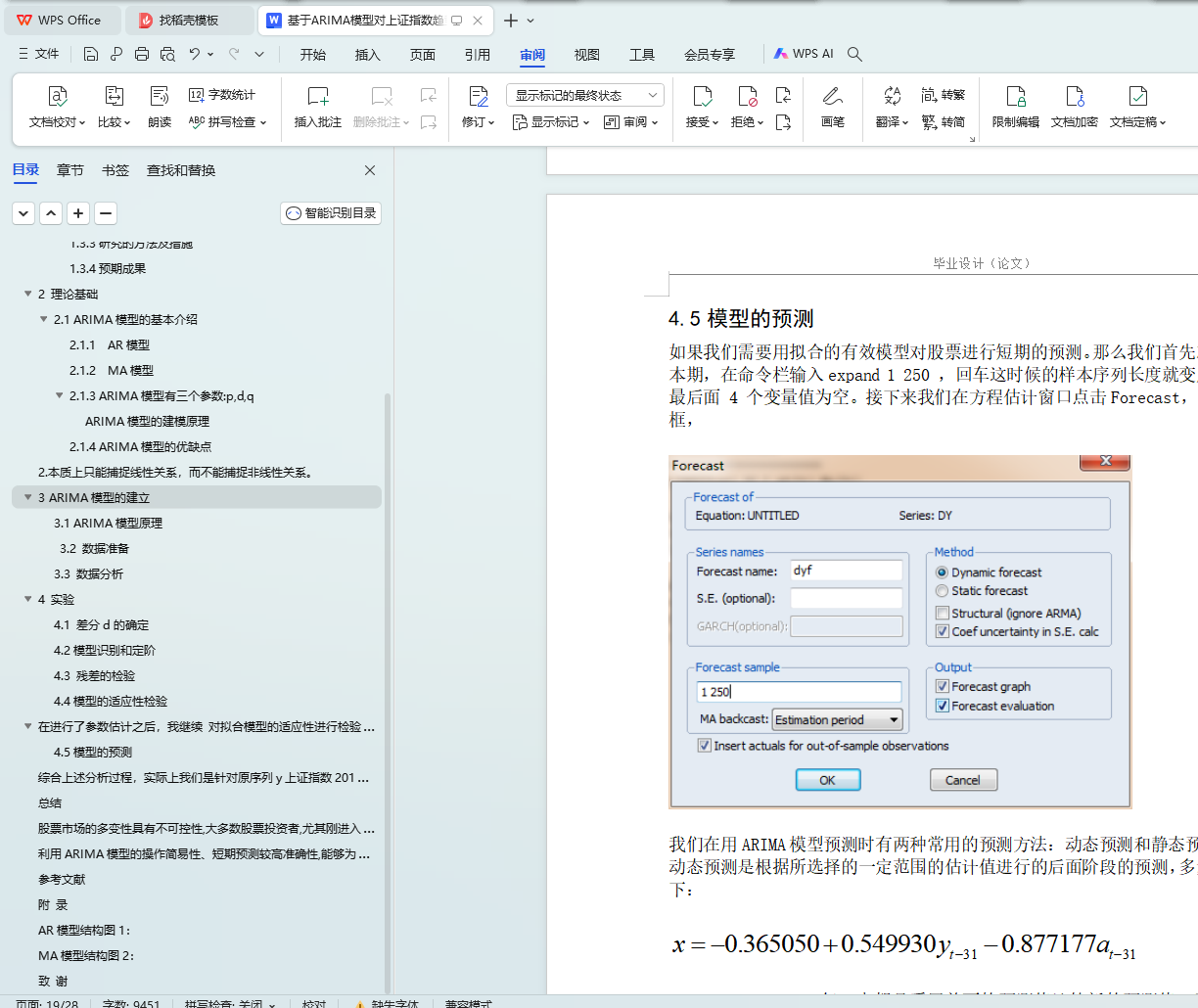

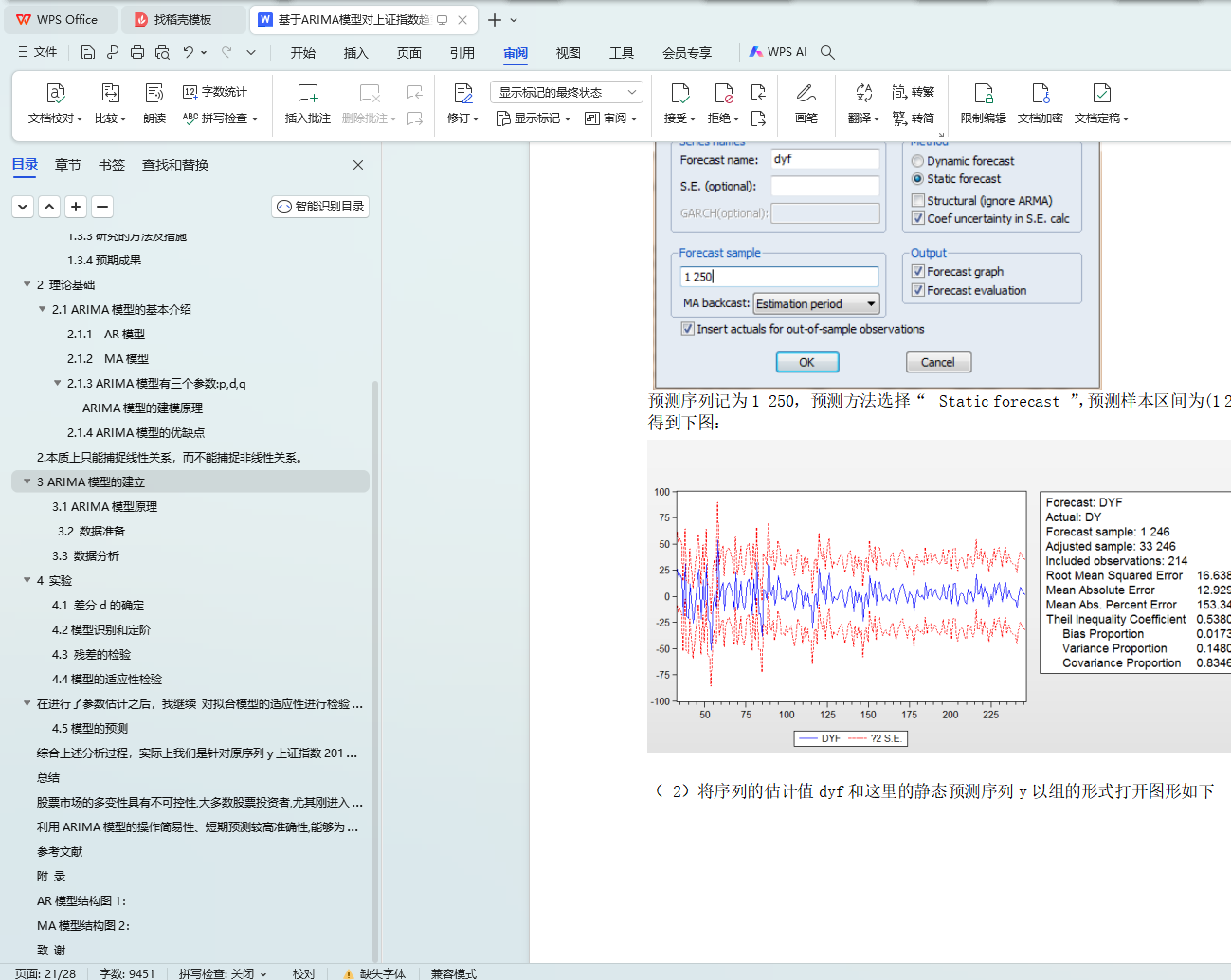

4.5模型的预测 25

结 论 26

参考文献 28

致 谢 30